Note: All information and commentary are as of March 31, 2022.

*Performance was miscalculated and was updated to reflect the current return.

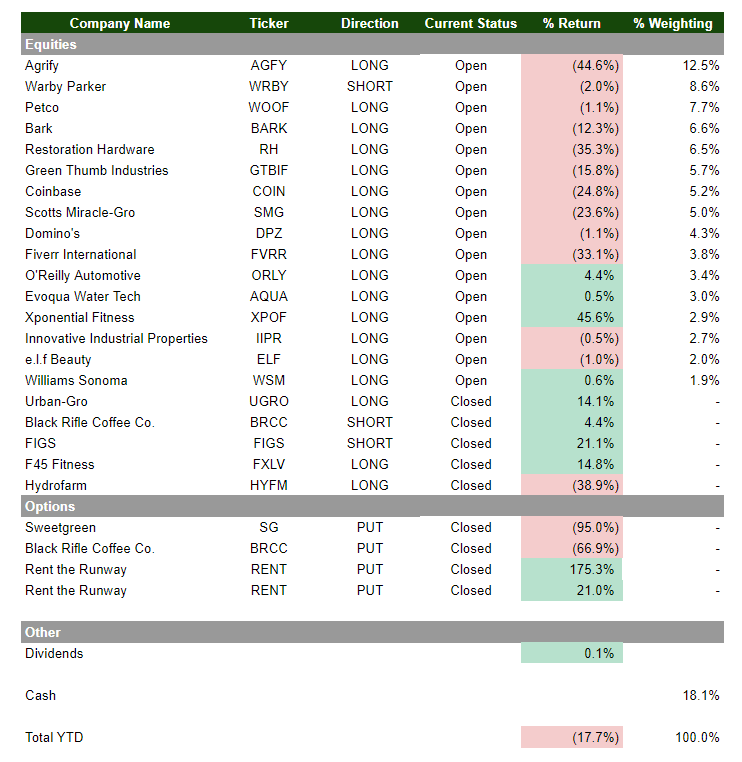

Fund Performance

In Q1 2022, Cedar Grove Capital Management, LLC (“Cedar Grove Capital” or the Fund” or “CGC”) returned -17.7% gross return compared to -4.9% for the S&P 500, -9.5% for the S&P Consumer Discretionary ETF XLY 0.00%↑, -18.5% for the Cannabis ETF MSOS 0.00%↑, -7.8% for the Russell 2000, and -6.0% for the Russell 2000 Midcap.

The Fund believes that its long/short strategy will deliver outsized returns in the long run, and that near-term volatility while creating portfolio fluctuations will allow CGC to take advantage of mispriced securities.

Portfolio Activity

During the quarter, we did have some opportunistic trades that helped offset some of the poor performance. These names are included below and the returns they generated during the quarter.

Other notable trades are listed below. As a reminder, our options contracts are more event-driven for target dates and never an overly sizable portion of the Fund’s assets.

Buys

New Positions

Warby Parker - WRBY 0.00%↑

Domino’s Pizza - DPZ 0.00%↑

Xponential Fitness - XPOF 0.00%↑

Innovative Industrial Properties - IIPR 0.00%↑

elf Beauty - ELF 0.00%↑

Williams Sonoma - WSM 0.00%↑

Added Positions

Agrify - AGFY 0.00%↑

Sells

Completely Closed

Urban-Gro - UGRO 0.00%↑

Black Rifle Coffee Co. - BRCC 0.00%↑

Figs - FIGS 0.00%↑

F45 Fitness - FXLV 0.00%↑

Hydrofarm - HYFM 0.00%↑

Sweetgreen - SG 0.00%↑

Rent the Runway - RENT 0.00%↑

Trimmed Positions

Restoration Hardware - RH 0.00%↑

Select Investment Commentary

The Fund has executed opportunistic trades that have offset some of the skimpy performance during the quarter, but there are a few names that I will highlight with additional color.

The Good

Xponential Fitness, XPOF 0.00%↑

Xponential Fitness is a boutique studio franchisor that recently went public in the back second of 2021. It operates ten fitness brand concepts across the US and has recently expanded its international footprint. We’re incredibly bullish on this post-covid fitness play and see a bright future for the company while already delivering a ~46% gain in a tough investing environment.

Our research on the name can be found here.

O’Reilly Automotive, ORLY 0.00%↑

O’Reilly Automotive is another favorite of ours. The company is an American auto parts retailer that provides automotive aftermarket parts—among other products—to service providers and DIY customers. We believe the company is an excellent compounder and will not only benefit from long-duration tailwinds, but also mitigate some risk in a potential future recession.

Figs, FIGS 0.00%↑ (closed)

Figs, a scrubs and lifestyle apparel brand, was a short of ours that started in November of 2021 on the premise that it was not the next lululemon for the scrubs industry. While we booked a gain of 41% on the name overall, FIGS realized a gain of 21.1% in the calendar year of 2022. Though our return was stellar, we left some money on the table with further market turmoil occurring into late January and into February. Overall, we are pleased with the result of this position.

Original research can be found here.

The Not So Good

Hydrofarm, HYFM 0.00%↑ (closed)

Hydrofarm, the #2 hydroponics player in NA, was one of the biggest single contributors to our poor performance in the quarter delivering a -39% loss. We were bullish on the name since last year, having expectations that they would be able to continue commanding a premium for their products in the cannabis space. However, growth slowly became more apparent through M&A rather than organic and the stock consequently sold off in the new year.

We have since closed the position and decided to double down on Scotts Miracle-Gro (SMG), the #1 hydroponics player in the US, which we still believe is deeply undervalued.

Original research/commentary for Hyrdrofarm and Scotts Miracle-Gro.

Restoration Hardware, RH 0.00%↑

Restoration Hardware, a retailer in the home furnishings market, was another major contributor to the Fund’s poor performance. The most recent earnings call by the CEO, Gary Friedman, was the shot heard around the world.

"I don't think anybody really understands how high prices are going to go everywhere, in restaurants, in cars and everything…..I wouldn't call it happy days right now. I'd call it pensive days. Be ready."

While many took this as a sign of future turmoil given that RH’s clientele is wealthy, we believe that the future is still bright for the company, and not the end of all days. Our thoughts from the ER can be found in the Twitter thread below.

With stellar growth over the last two years, margin expansion of over 1,100 bps, and its stock price cut by over half since November, we believe that while near-term price action could send the stock lower, long-term the stock is still a winner.

International expansion is just in the early innings with its UK location opening soon, and the company’s push into more luxury hospitality to go alongside its high-quality products. While we did trim some after the ER, we will look to buy more when the dust has settled with the name.

Recent research can be found here.

Agrify, AGFY 0.00%↑

Agrify was a darling in 2021 having risen ~200% since its IPO early last year. Since August, the stock has been struggling with many investors becoming risk-off in light of changing macro environments and a short report that came out in December of 2021. While we believe the short report brought up some good questions, overall the piece had many holes.

Unfortunately, the company did not address the short report as they felt that it did not hold weight and instead shared commentary with the sell-side analysts rather than make a public statement. We believe this lack of acknowledgment or denial of the report set the stage for further price turmoil in the stock where it’s traded well below its IPO.

While this is obviously not ideal, the company is still expected to grow topline by triple digits after having just ended FY’21 with +395% growth. Cedar Grove Capital believes that while there are many factors hindering the company’s retracement upwards (being a micro-cap stock , short report, macro environment, market liquidity and lack of coverage), the future is still bright for the company and patience will be key.

Original research can be found here.

Sweetgreen, SG 0.00%↑

Sweetgreen unfortunately was a recent short idea of ours and we miscalculated the cult following that the company had. While we had put contracts that were up 60% going into the print and were positioned to perform nicely once earnings came out, the company announced a surprise beat on revenue and raised guidance with the possibility of lighting less money on fire.

While at face value this looked as if it was as bad as everyone thought, investors still ignored the red flags and pushed the stock up an absurd 82% in two weeks from the lows and eventually settled only up 50% since the print to end the quarter.

While our put contracts were deemed worthless, they were a small portion of our assets. We still believe the company is overvalued and are patiently waiting for another opportunity.

Original research here.

Thinking Ahead

For the first quarter of 2022, many unpredictable events occurred that sent the markets into a freefall. With the invasion of Ukraine by the Russian Federation, commodity prices in many categories (oil, wheat, fertilizer, etc.) have directly affected a few names in the Fund in a meaningful way.

Aside from the invasion, FED policy in combating record inflation might become more aggressive than anticipated, thus the cost of capital is expected to rise dramatically.

Given the industries that Cedar Grove Capital invests in, this coverage exposes the Fund to cyclical trends in the overall market though it creates opportunities in niche areas that the Fund can capitalize on.

With 16 positions in total (15 long, 1 short), the Fund has utilized one percent of its margin buying power and is sitting on 18% of its cost basis in cash. Given the amount of dry powder available to deploy, areas of opportunity for the Fund to expand or double down on can be found below:

1) Restaurants

Despite inflation and labor shortages, there are names within the restaurant space that have shown to be resilient to these challenges while also proving to have strong pricing power. This resiliency will help them weather the near-term storm while coming out a strong winner.

2) Automotive

Even with the rapid adoption of EVs, traditional ICE vehicles will still need to be serviced and there is evidence of not only growth in the ICE space, but a longtail to support sustained growth in the overall industry.

3) Consumer/home goods

With select C&R names having been beaten down since the start of the year, there lies an opportunity to invest in some companies that are still benefiting from consumer discretionary spending.

4) Select cannabis

While the traditional cannabis market is tough and hard to invest in, there are underlying companies that support the growth of the industry and do not face the same challenges as pure-play cannabis companies.

5) Fitness

In the post COVID world of fitness, hybrid workouts are what the future will entail, though there are some names in the space that are still benefiting from in-person exercise. We believe that Xponential fitness is one of these names.

While the Fund currently only has one short position and net long exposure of over 90%, we will continue to look for and identify names that we believe the market is mispricing. The recent uptrend from mid-March seems to have strong support to run higher, thus we will be looking opportunistically and with patience.

Some names that we have wanted to execute on in the past have consequently had a high cost of borrowing rate and kept us away from starting a position. Should this change, you can expect to see more short positions over the next few quarters.

Closing Remarks

The first quarter of 2022 has been a difficult one and we are not alone in that. Luckily, given our thematic strategy and our investors’ understanding that some of our ideas will take time to develop—notably in the cannabis space—many of our positions will prove fruitful in the long term.

The Fund will continue to evaluate positions as new macro data continues to be released, and will strategically identify potential short positions in key cyclical areas. With so much cash to use, more opportunities will continue to arise. Some of which we have already begun to see.

Until next time,

Paul Cerro

Q1'22 CGC Quarterly Letter