Summary

Once a VC darling, this “tech” oriented restaurant chain is anything but

The company is not differentiated and some aspects of its business expose it to more risks than others

Higher inflation and lack of pricing power will continue to eat into the company’s margins

Widening losses and no path to profitability should make investors wary of where the company’s priorities are

Compared to other restaurant brands out there, that are profitable, valuation metrics show just how overvalued Sweetgreen is

Business Overview

Sweetgreen SG 0.00%↑ develops and operates fast-casual restaurants serving healthy foods prepared from seasonal and organic ingredients and serves customers via 140 stores across 13 states plus D.C. They sell their goods through two channels; in-store and digital.

Menu items offered include signature salads, warm bowls, and plates that are complemented by a seasonal menu that changes five times a year.

Restaurant Count: Increased from 29 restaurants as of the end of fiscal year 2014 to 119 restaurants as of the end of fiscal year 2020; 27% CAGR. As of September 26, 2021, They have grown to 140 restaurants.

Average Unit Volume (AUV):

2014-2019: Increased from $1.6 million to $3.0 million; 12% CAGR

2020: $2.2 million

2021: $2.5 million as of September 26, 2021, compared to $2.3 million as of September 27, 2020

Financial Overview

When it comes to restaurants, there are really two views that you have to be mindful of when looking at their financials

Overall sales and costs - this is for the entire company, holistically

Restaurant-level sales and costs - this shows you how well on just a restaurant-level the company is doing. This removes all costs not associated with running the restaurant on a daily basis and also highlights how well the restaurants are doing

Let’s start with the high level, how well is SG doing as a “company.”

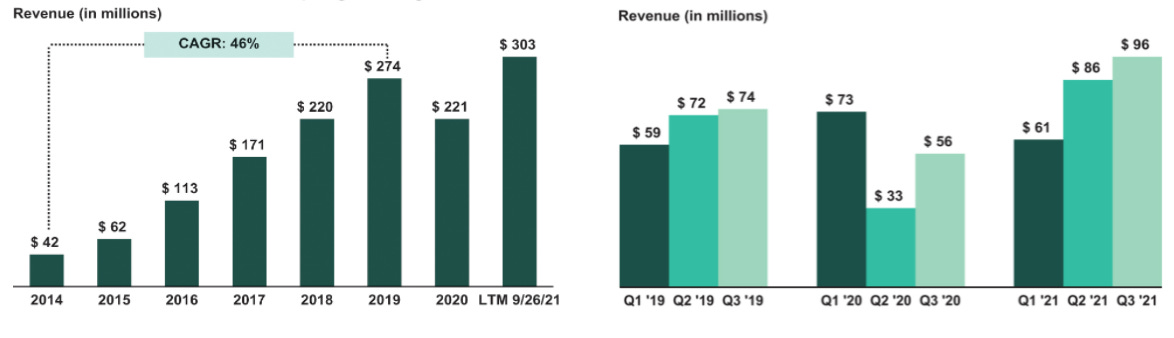

Net Revenue:

2014-2019: Increased from $42 million to $274 million; 46% CAGR

2020: $221 million

2021: $243 million for their fiscal year to date through September 26, 2021, compared to $161 million for their fiscal year to date through September 27, 2020

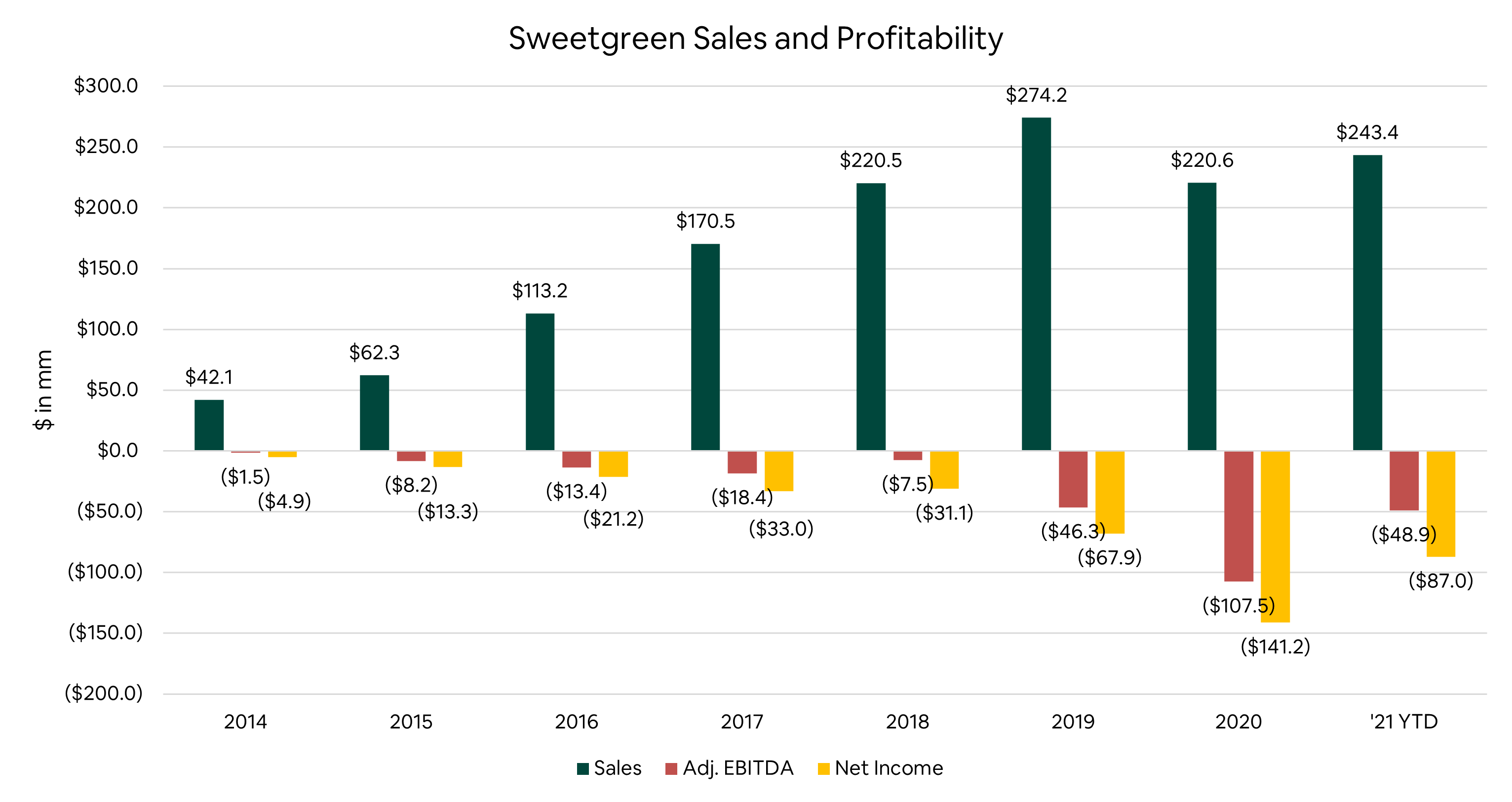

Loss from Operations:

2014-2019: Increased from ($5) million to ($70) million

2020: ($142) million

2021: ($87) million for their fiscal year to date through September 26, 2021, compared to ($100) million their fiscal year to date through September 27, 2020

Restaurant-Level Profit:

2014-2019: Increased from $8 million to $44 million, representing a Restaurant-Level Profit Margin of 16% for fiscal year 2019

2020: ($9) million, representing a Restaurant-Level Profit Margin of (4%)

2021: $28 million for their fiscal year to date through September 26, 2021, representing a Restaurant-Level Profit Margin of 12%, compared to ($6) million for their fiscal year to date through September 27, 2020, representing a Restaurant-Level Profit Margin of (4%)

Financial Targets

Year two Cash-on-Cash Returns of 42% to 50%

AUV of $2.8 million to $3.0 million

Restaurant-Level Profit Margin of 18% to 20%

An average investment of approximately $1.2 million per new restaurant

Recent Stock Performance

Sweetgreen (SG) opened 85.7% above its $28-a-share IPO price on November 18th of 2021 and quickly rose to as high as $56.20, up 100.7%.

The IPO valued Sweetgreen at some $3B on a non-diluted basis even before the IPO pop. The sharp first-day rally boosted that to about $5.3B and the company effectively raised $364 million from the IPO.

Since then, with news of omicron and the FED deciding to begin tapering, the stock sold off from its highs and has been trading in a band around the $25 - $30 price range.

Thesis - SHORT

Believe it or not, I actually like Sweetgreen salads. I think they taste great and have a lot of different kinds of ingredients that allow them to create awesome bowls. However, I only had Sweetgreen on a regular basis because Merrill Lynch paid for my dinners back when I was a banker, otherwise, no way I was paying over $15 a day for salads (more on this later).

But before I dive into why I have decided to short them, let me briefly go into what the company is doing well since they aren’t a “bad” company at all.

What’s Going Right

Sales, stores, and AUV growth

Like I showed you before, revenues for the company, which coincide with the number of restaurants added, continue to grow over the years. Jumping from $42 million in sales with 29 restaurants in 2014 to $243 million in sales and 140 restaurants YTD in 2021.

This is great and considering that 2020 was an obvious off-year, AUVs have steadily increased to $3 million in 2019 with YTD 2021 posting AUVs of ~$2.5 million.

Additionally, the company plans to double the number of restaurants that it owns over the next three to five years bringing the total figure to just shy of 300 total units.

New strategies

Expansion of digital

It’s important to note that more than two-thirds of Sweetgreen’s revenue comes from digital sales.

While you could order Sweetgreen online for some time, the company has recently expanded its store’s optimization to accommodate for increased digital orders. This means that there are lines for in-store ordering and for digital pick-up. This allows them to handle more order volume without adding more costs or square footage. Additionally, it enables them to quickly take advantage of the rising demand for off-premises dining.

New restaurant formats

When COVID erupted and prompted everyone to not be able to eat indoors, pick up or delivery were the only options. Some restaurants quickly retrofitted their existing stores to incorporate drive-thru options and park and pick up to speed up delivery times and encourage consumers to get back out and order their food with limited risk.

As Sweetgreen expands from its coastal, and urban environments, more locations will be adding drive-thru and pick-up only options.

Large balance sheet no debt

Surprisingly enough, Sweetgreen does not have any debt. Given that they were a VC darling prior to going public, they kept raising through traditional private markets and have expanded without dipping their toes into taking on leverage.

Prior to going public, they had $137 million in cash on the balance sheet and raised an additional $364 million from the IPO. So they have no risk to FED raising rates (at least not directly) and a large war chest to help them expand during their growth phase.

Why I’m Shorting

The company is doing great, but at the end of the day, they sell expensive salads. The reasons I’ll address as to why I decided to short will be in relation to

The story that they’ve sold investors

Limited TAM

Lack of any differentiation or moat

Increasing ingredient and labor costs

Local sourcing

Work from home

Profitability

1) “It’s a tech company”

Its IPO prospectus filing reads part health-food brand, part technology startup. If you do a search for “technology” in Sweetgreen’s S-1, you get 89 references to that word. Spoiler, many of them have to deal with how they “leverage” technology to drive growth.

When I kept seeing this, I kept getting flashbacks to Adam Neuman pitching WeWork as not a real estate company but a “technology” company. Adam, you were renting desks and Sweetgreen is just selling salads. No one is reinventing the wheel here.

However, in the hot land of Silicon Valley, this did not deter VCs from valuing the startup at $1.78 billion before going public.

So aside from it being an actual “tech” company and just utilizing digital ordering, there’s one specific example as to why many might believe in that narrative.

Spyce Acquisition

Spyce, founded in 2015, is a Boston-based startup that started making waves a few years back as a spinout of MIT mechanical engineering students. First serving up food at the school’s dining hall, the team ultimately opened a pair of automated restaurants in the Boston area.

I’ve included a video below for you to check out and see exactly for yourself what they do.

In a nutshell, Spyce utilizes technology within restaurants to fulfill customer orders on a made-to-order basis while ultimately being able to cut out most labor costs. Basically having robots make your food perfectly every time without the need to pay workers to do it.

While this most likely will be the future of certain types of restaurants, in reality, that is a very distant future and investors should not be applying a premium on the company now because of it.

2) Limited TAM

I love reading S-1s and consistently seeing how big the total addressable market (TAM) is. Almost all the time it’s pretty laughable.

Sweetgreen’s is particularly laughable because they start at the tippy top of the total food market valued at $1.8 trillion and then don’t even address the actual size of the healthy food market but just highlight how it’s grown at a 9% CAGR from 2010 to 2019.

LOL, okay…

Despite them not even knowing how big their market is, I will give them the benefit of the doubt that the market for healthy eating is in fact growing. However, this is negated just from the pure reason of how expensive their salads are and who can afford them.

Two points to this.

One is where they operate stores and the other is pricing. If you look at the map below, many of the current restaurants are in the coastal areas of the US or in urban cities.

Not many suburban restaurants currently exist but if the company plans to double its footprint in the next three to five years, the biggest question that needs to be asked is can they resonate with suburban areas? Will suburban consumers want to go out of their way to order a salad from Sweetgreen?

This question is a lot easier to answer in urban areas for various reasons but then the second point is, are they willing to pay premium prices for these salads?

My guess is probably not, and to add more color on this as well, if the company wants to attract this type of consumer, then prices will need to drop significantly compared to urban areas, thus, driving down overall AUVs.

3) Increased costs + lack of pricing power

Okay, so this is going to be the first time I reference Chipotle (CMG) in comparison to Sweetgreen. The reason I bring them up is that they are the closest pure play company to SG that we can relate to.

So with this being said, what does increased costs and pricing power have to do with CMG? Well, it was all in their earnings call.

Firstly, we all know that it’s getting harder to hire people for these types of jobs and also, the costs of goods are going up. CMG was able to offset this with price increases.

CMG hiked menu prices by 4% in December, citing commodity inflation elevating beef and freight costs, and, to a lesser extent, avocado.

Chipotle CEO Brian Niccol said,

…the restaurant’s prices were around 10% higher than a year ago, adding that further increases could come if elevated costs don’t abate.”

“We’ve got a lot of pricing power”

This is great for CMG but it highlights two things that directly relate to SG.

Costs are going up for everyone

Price increases need to happen to retain margin

The first is easy because that’s expected to happen but where I think Sweetgreen will fall short is their ability to raise prices. It’s easy for Chipotle to raise prices because naturally, rice and beans are cheaper. Their bowl in NYC was going for ~9.50 (no additions) and now ~$10.50. The number of people that can still buy this on the regular is a lot.

However, Sweetgreen’s average salad cost in NYC is ~$15, and if you’re ordering for delivery, that only goes higher. It’s hard enough for people to rationalize spending $15 for a salad already, do you think they want to spend more? My assumption is no.

Without being able to raise prices that much and not deter customers, costs will eat into margins and put more pressure on its bottom line.

4) Lack of differentiation or moat

Salads aren’t anything new and arguably “artisanal” salads aren’t new either. The market is filled with incumbents who offer fresh and healthy meals and other health-conscious new entrants that add more optionality to consumers to choose from.

I could list all the healthy food chains out there that number in the thousands of stores at this point but I’ll spare you from the incredibly long list.

With just 140 store locations, Sweetgreen is a minor player in a very fragmented, large, and competitive market.

When it comes to “leveraging technology,” yeah that’s not anything new at this point it’s practically table-stakes when doing anything in the food industry. The digital ordering I mean.

So with nothing different about what kind of food Sweetgreen sells or how people can order, it’s just another fast-casual restaurant pumping high-priced salads.

5) Local sourcing only sounds good

Being able to brag about how your ingredients come from local sources only sounds good. In actuality, it’s quite expensive and puts the company more at risk than need be.

David Trainer from Value Investing 2.0 said it best in the comment I added below.

Unlike McDonald’s, and other more established restaurants, which enjoy economies of scale from a vertically integrated supply chain, Sweetgreen focuses on sourcing its food locally. To do this, Sweetgreen typically relies on a single, regional third-party distributor for fresh products and another regional distributor for dry goods. By not utilizing national distributors, Sweetgreen adds complexity to its supply chain, which makes it more difficult and potentially more costly to manage. For instance, Sweetgreen has more domestic food partners (200) than restaurants (140).

Chipotle, which offers its own variation of a salads relies on more traditional large-scale food suppliers which helps the company better manage costs. In 2020, Chipotle locally sourced only 11% of its produce from 54 local farmers to serve its ~2,900 stores.

This relative inefficiency leads to higher operating costs. Sweetgreen’s restaurant operating costs increased from 84% of revenue in 2019 to 88% of revenue in the nine months ended September 26, 2021. Chipotle’s restaurant operating costs, on the other hand, were just 77% of its food and beverage revenue in the nine months ended September 30, 2021.

Will being locally sourced help the company in the super long term? Perhaps, but it will take Sweetgreen some time to get there before that realization can be recognized. To make matters worse when you have that many partners sourcing your food, it adds risks.

Pulling further comments from David on the matter.

Relying on numerous third-party sources makes guaranteeing that quality control standards are maintained throughout the supply chain more complex.

A lack of control over its supply chain exposes Sweetgreen to even more risk than other types of restaurants as it serves large amounts of uncooked food, which is more susceptible to foodborne diseases. In 2019, when Sweetgreen received reports from New York City customers about illnesses caused from spoiled blue cheese from a local supplier, the company had difficulty tracing which restaurants received the spoiled product. As the company grows its store footprint, its ever-increasingly complex supply chain could expose its customers to riskier food.

We’ll see if they can actually scale this as their stores continue to grow but their model of not operating under similar practices of large-scale restaurant chains is uneasy.

6) Working from home is a problem

Sweetgreen’s business has largely been fueled by office workers, many of whom will now be able to work from home permanently. Before the pandemic, Sweetgreen had more than 1,000 Outposts – drop-off points for offices, residential buildings, and hospitals – that delivered meals to consumers on a regular schedule.

Sweetgreen notes in its S-1 that

“Outpost customers have been our most habitual users, with the average Outpost customer ordering approximately six times per quarter.”

Nearly all of its Outposts were closed in 2020 as offices closed during the pandemic. While the number of Outposts rose to ~35% of pre-pandemic levels in Q3’21, it’s hard to think that the fates of in-person work and Sweetgreen aren’t intertwined, even as the popularity of delivery apps and ghost kitchens grows.

Decreased Outpost sales mean lower sales per store for Sweetgreen.

7) Profitability

If you didn’t notice the financials that I posted towards the top of this article or the breadcrumbs along the way, let me ask you then how much money you think Sweetgreen makes from its high-priced salads?

The answer is none, technically, less than none, because it’s negative.

In its S-1 filing, the chain reports that despite serving more than 1.3 million customers in the 90 days prior to its filings and raking in revenues of more than $300 million in the last twelve months, Sweetgreen is not a profitable business — and it’s unclear when it will be.

The company blames the pandemic for lower revenues in 2020, but the company is also burning tons of cash as it pursues both growth via new restaurants and making acquisitions like Spyce.

What’s funny is when you compare Sweetgreen’s IPO to Chipotle’s. In 2006, when Chipotle went public, they were actually profitable since 2004. If you look at Portillo’s PTLO 0.00%↑ that recently went public, despite a terrible stock decline, they were also profitable and even during 2020’s pandemic!

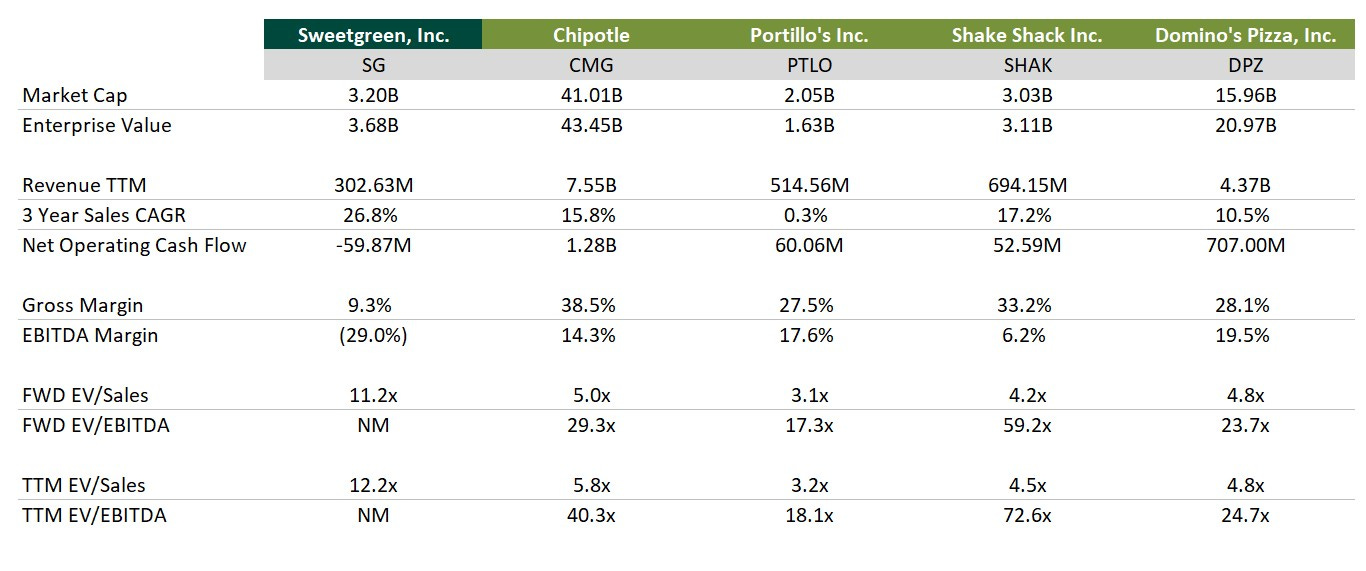

But to give you a better picture, let’s look at the metrics that we can compare with other restaurant players.

Valuation is too rich

When we compare Sweetgreen to others, it doesn’t look pretty and that’s really the foundation to why I looked into shorting it in the first place.

I’ve decided to compare SG to four other companies: Chipotle, Portillo’s, Shake Shack, and Dominos. All of these companies have a) digital component, b) aside from Domino’s, the others are company-owned and not franchised, and c) they operate in different parts of the country if not all around the country.

There’s a lot to unpack from the above chart but the main points that I want to drive home are that while the company is growing topline faster than its peers, it misses on a few key metrics and trades well above its peers.

Take a look at Shake Shack (SHAK) for example, it has an EV of ~$3.1 billion, has more than double LTM sales of SG, is profitable on an EBITDA basis, has better gross margins yet trades at 4.5x forward EV/sales compared to 12.2x for Sweetgreen.

I’ll leave you to take a look at the chart to compare against the others but let’s value the company based on comparable metrics.

Since Sweetgreen doesn’t even have positive free cash flow, we can only value it on a sales multiple. Using these four comparables, and FY2022E sales of $511 million, we can get a share price of $22.70 via using the median multiple, or $21.61 via the average, representing a 26% and 29% downside from yesterday’s closing price.

While I have covered other companies in the past using sales as the valuation metric, it’s tough to back that up in a now quickly anticipated rising rate environment. I can’t even project adj. EBITDA because there’s no clear pathway to becoming profitable at the rate that they’re spending (LTM capex of $73 million).

Even using this multiple is giving them the benefit of the doubt that they are even on par with the other companies despite lower GM, no earnings, negative FCF, and a track record that shows that their bottom line is only getting worse.

Closing Thoughts

While I like the company, I hate the stock, and that’s not the first time I’ve said that.

At the end of the day, the company sells expensive salads and is still losing money.

The only real highlights for the company are all based on the topline growth (sales, restaurants, presumably AUVs) and fail to comment on how they’re addressing the widening losses that they are experiencing as if they expect to have endless access to capital.

With negative operating cash flow but a large cash balance, I think it will be some time before they will need to raise money but given the share price fall, I would expect insiders to share their stock once the lock-up period expires.

Either way, other restaurants that are doing much better than them are trading for a lot less and that’s for good reason.

One thing to note that will move the stock in either direction is when they release earnings for the very first time since going public on March 3rd.

Until next time,

Cedar Grove Capital

Sweetgreen: Serving Green But Bleeding Red