TL;DR

Petco’s omnichannel push will help it solidify itself as top pet health and wellness company with a strong defensible moat and loyal customer base

Continued push into value-added services creates a closed-ended one-stop-shop ecosystem for all pet owners

Its strategic initiatives will drive top-line growth and significantly improve the company’s profitability and cash flow

Given the company’s strategic growth initiatives, the market is mispricing the potential for Petco to deliver outsized returns over the next few years

Petco Health and Wellness WOOF 0.00%↑ is a pet supplies store that offers a range of products from toys, treats, and food all the way to grooming services, vet care, and pet insurance. I actually wrote about them before on April 1st and you can read about it here.

The company operates approximately 1,500 pet care centers across the U.S., Mexico, and Puerto Rico, which also includes a network of more than 100 in-store veterinary hospitals.

So how does a pet supplies company positioned to deliver upsized returns? It all starts with what they’re on a mission to build.

End-to-End Ecosystem

Petco has (personally) been a misunderstood company. It was taken private and only recently went public early last year. Still, many have written it off as just a traditional large retailer that a) is a slower growth with no real catalysts and b) whatever benefit it had during COVID was a pull forward and that’s that.

But what many fail to realize is that while Petco had been point A for quite a while, management under Ronald Coughlin has really revamped what it traditionally used to be. Ronald has focused on two main parts of the business:

Leveraging retail footprint in their favor

Moving into pet health and wellness

As simple as they are, these two main parts, are part of a broader strategic play of building a fully encompassed end-to-end ecosystem. A true “one-stop-shop” for all pet parents.

With that said, let’s better understand the overall business with point A.

Retail

Retail is a the forefront of what the CEO is using for his plan. Once labeled a liability with the “death of retail” narrative years ago, many have pivoted to using their square footage to help drive sales alongside their digital footprint. What do I mean by this?

Well, traditionally, it was either a) we go in-store and buy the goods or b) we can wait and order online.

The latter obviously is more convenient for the customer since all they have to do is order and wait but adds to the costs for the company (Petco) since S&H costs so much, especially if it’s heavily weighted dog food, etc.

Petco has taken a different approach to this in order to fight back against compressed online margins and even incentivize the consumer to come in and physically pick up their order. Let me dive into each of the components and how each fundamentally helps the overall business grow stronger and better.

Petco App Drives Sales

The first thing is Petco’s drive into the digital age. Having been slow to build out this functionality, it’s quickly catching up and reporting great numbers from all the spending it’s been putting into it. For instance, their app is a great driver of sales for them, having been downloaded 5.7M times since its launch, its app-generated revenue and active users have almost doubled from Q4 of last year.

What’s great to hear is that Petco’s app customers are quite valuable to them. They typically spend almost 2x that of customers that don’t use the app which means that they contribute to higher digital sales and bigger basket sizes. Check in the digital win column.

BOPUS Incentive

For context, BOPUS = “Buy Online and Pick Up in Store”. In a world where it seems to order online and having it arrive at your door is as easy as ever, how can you change that force of habit to be in your favor? Well, give people an incentive.

That’s where BOPUS comes in. This incentive can be purchased online or through their app and offers the customer a certain percent discount off their order (usually requires a minimum spend) to just come in instead of having it shipped to their door.

Sounds simple enough and that’s cause it is. Just look at the quote pulled from Petco’s Investor Day below.

And if you look at same-day delivery, BOPUS, we have 50% lower cost when we ship through our pet care centers, 50% lower cost using our structural advantage. And here's the part that blows my mind. When we make BOPUS and same-day delivery available to our customers, they are choosing it 91% of the time. Our customers love what we can uniquely offer.

This directly aligns with the company using its physical footprint as leverage to drive sales but also save on margin from not having to pay on shipping (mentioned above). The unit economics of this plays out well for the company and the consumer leaves happy after receiving their discount and getting it faster than shipping.

To generally note on top of this is that it’s widely known in the retail landscape that when customers physically go into a store, they spend more on average. I’ve had plenty of times where I’ve used BOPUS and then I see something else and buy that too.

A small incentive helps save on margin but then doubles as another way to increase sales once the customers come in. Genius.

Same-day Delivery - DoorDash

Having recently launched last year, Petco has thought of ways to really push its agenda on a full omnichannel approach. Historically, dealing with two ends of the spectrum (going to pick it up or ordering for delivery) was limited. But what if you could find a happy middle? Petco did. They partnered up with DoorDash in order for pet owners to be able to buy their goods online but still have them delivered the same day, for no extra charge (requires minimum order + optional tip).

To highlight this advantage, the company gave an example of what this brings for the company.

We've created structural advantages versus online-only competitors. Let me give you my favorite example on this. This tennis ball on DoorDash costs us the exact same to get to a customer as a 40-pound bag of dog food. This tennis ball cost the same as a 40-pound dog -- bag of dog food in DoorDash. That's a generator of competitive advantage.

Another check for margin.

Additionally, this partnership only had a one-time window - order by 2 PM and get it the same day. Recently announced on their investor day, Petco is now moving from one same-day delivery window to 4 same-day delivery windows throughout the day.

*Value creation*

Repeat Delivery

One of the biggest online pushes, broadly speaking, is the idea of repeat orders. The premise is easy to understand, set some products for a regular delivery cadence and you can get a certain percentage off of the order by doing so (typically 5-10% on average). By doing this, you as the customer get the benefit of not forgetting to order goods and a slight discount by doing so (I do this for my pet - crazy convenient). As the company (Petco) you get the added benefit of recurring revenue which is easier to account for and a steadier understanding of inventory for supply chain and logistics purposes.

Now while this has existed over the few years, Petco is taking it one step further.

Our repeat delivery business, it's one of the highest retention rate businesses that we have. And what's great is that later this year, we're actually going to be offering it inside of our pet care centers. And our data suggests that when we do that, we double the spend of our customers, and we do it without taking nearly any revenue or profit out of our pet care centers.

It’s ideas like this that will help continue to contribute to the company’s top-line growth while expanding on margins.

Private Label

Speaking of margins, Petco is big on offering a lot of private-label goods (Whole Hearted, Well & Good, Reddy, etc.). Private label brands help companies with margin because they themselves own the supply chain (in most cases) to bring those goods to market.

The majority of our portfolio cannot be found at Safeway, it cannot be found in Walmart, cannot be found in Amazon, it cannot be found at Chewy. If a customer wants Friskies or Pup-Peroni, they can go to dollar stores, they can go to supers, they can go to our pet specialty competitors because we're not going to compete for that commoditized, low-margin business. What we're focused on is power owned brands, building power owned brands and putting underneath them differentiated offerings.

Having customers shift from say, Blue Buffalo dog treats to WholeHearted dog treats, will deliver sales (with a possible haircut) but the margin is much bigger in comparison to name brands, as mentioned above.

Fresh Food

Given that many pet owners treat their pets as if they were their own children, giving them the best life we can sometimes entail what we feed them. The push for premium fresh food is actually growing and the market is set to more than double in size by 2025.

Petco takes advantage of this trend by offering a few options - JustFood For Dogs (exclusive to them), Instinct, and FreshPet. So far, the company has achieved 2.6x customer spend with more trips to their centers to pick up the food leading to higher baskets.

The company realizes this trend will continue to be beneficial and plans to grow JustFood For Dogs to over 1,000 pet care centers and even plans to launch its own private-label fresh and frozen options through WholeHearted.

Pup-box

Pup-box is a subscription box offering that Petco has been nurturing for some time now that sends pet owners a box of goods and treats for their puppy. Think Bark Box but for puppies.

Historically, the company offered this service just to puppies but now has expanded to adolescent, adult, and senior boxes. While this isn’t a huge driver of growth, it is important to note this as another driver of value that the company is doing for its customers.

Services

The second part of the company’s push in the pet space, point B, is with its services. While you can do your best to grow the retail footprint (which they have) the real long-term win here is services.

These services can exist both in and out of the store but are lucrative in their own way. In fact, Petco saw a jump in their “services and other” category by 43.2% YoY to $670M in FY’21. It’s currently their fastest-growing segment followed by consumables.

Let me explain how through each one.

In-Store

A few in-store services that the company has been expanding on involve grooming, training, veterinary, and adoption services. These services, while not big in nature, help build out the ecosystem that management has been aiming for. At the very pet care center that your get your pets’ supplies from, why not also go in to get them trained, groomed (usually a regular cadence), or adopt one.

Training services are very important and I remember over 1.5 decades ago getting our first family dog trained by them because we had no idea what we were doing. We also used them to groom our dog as well.

Looking at overall TAM sizes

Grooming - $6 billion by 2026 growing at a 5% CAGR

Training - $1 billion in 2020 growing at a 6% CAGR

Veterinary - $34 billion in 2021 growing at an 8% CAGR

A quick stat about these services as well for Petco

…over 50% of our appointments for services that includes vet, grooming and training are done on our online platforms and primarily on our app, increasingly on our app. So the digital marriage of our of our services business, I think, has been one of the big, big game changers for us over the past couple of years. And when you think about it, we talk about this all the time, most of our competition is smaller proprietors who just do not have the marketing or the technology capabilities that we'll bring to bear.

The stickiness of its offerings is really helping drive traffic which then further reinforces my previous point about incremental in-store sales once you get the customer in the door.

Health & Wellness

Amongst pet care services mentioned previously, the health and wellness part has the biggest market potential and is the one I’m most excited about in terms of growth.

Veterinary services

Vet services is a growing service that Petco has decided to capitalize on. With the pull forward in pet adoption during COVID (3.3 million pets), long-term care will be needed for them and the continued adoption of pets.

So far, Petco has built 197 animal hospitals in care centers called Vetco Total Care and plans to scale to about 900 overtime. Historically, the company has mentioned a 70 annualized target. Even from the company’s S-1, the CEO mentioned

“Notably, our hospitals completing the third year of operations are ahead of model, generating over $1 million in revenue and over $200,000 in four-wall EBITDA in year 3.

Pharmacy

Aside from receiving treatment services for your pet, the other part of this equation is the medication that goes along with it. The most common medications that everyone is familiar with are flea & tick and heartworm medication but pharmacy fulfillment goes well beyond that. In total, the U.S. pet medication market was valued at $10.8B in 2020, up 19% from 2019.

The pet medications market not only navigated the COVID-19 pandemic but continued to thrive, given the increased focus on pet health and wellness and the surge in pet adoption and acquisition brought on by the pandemic.

Pet Insurance

So just like humans, pets can have insurance too and the cost to insure a pet, unfortunately, comes directly from the owner and is not company sponsored. With that being said, companies that operate in the space can command high premiums for your pet, and based on the plan you select, they can fluctuate with the level of copay and deductible you choose.

Overall, pet insurance is important for the average pet owner since over the life of a pet, veterinary expenses for a lucky vs. unlucky pet can vary from $500 to more than $50,000, according to Trupanion. So while Petco is operating the vet clinics/hospitals, they can leverage the service offering to pair it with their own pet insurance.

According to IBIS World, the pet insurance business is estimated to be worth $2.5B in 2022 and will continue to grow at a CAGR of 9% annually to 2027. While this is down from the ~16% CAGR from 2017 to 2022, the absolute figure is still impressive.

What’s also great to note about pet insurance is that it is billed on a monthly cadence. Just like I previously mentioned above with Petco’s repeat delivery and Pup Box, pet insurance creates an additional recurring revenue stream. Additionally, pet insurance is a great example of creating a flywheel effect where many owners will spend a lot on their pet upfront (a loss to insurers at the start) to care for their pet that over time, this spend tapers off as this creates better health outcomes later in life.

Though the pet insurance business is a nice feature to add to Petco’s value proposition, it is not meant to be a big cash driver for the business until much later in its maturity. For the time being, we see pet insurance as a nice additional sticking point for pet parents looking for solutions that can also be fulfilled from the same place they also get other goods or services.

Until then, we are counting on it being more of an acquisition tool (just like veterinary services).

Pal Rewards/Vital Care

The last offering that brings this all together is their Pal Rewards program and Vital Care. Pal Rewards is just a points-based system that you earn based on how much you spend which is assisted by the 24.1 million total active customers Petco has. Nothing crazy, just a typical rewards program. However, the company generates over 80% of its sales from its Pal Rewards members.

If we pivot over to Vital Care (a premium membership offering with ~1.2M members) the perks that go along with that are great. For $19.99/month, you get:

A $15/mo Pal Reward

10% off any brand of dry, wet, fresh, or frozen nutrition (excludes treats and chews)

20% off every groom (typical full price of ~$60 excluding upgrades)

Extra 5% off repeat delivery nutrition

Unlimited routine vet exams ($20 Pals Rewards for every routine exam at the vet of your choice or unlimited routine exams at all Vetco Total Care locations.)

With just the first two bullet points, you’ve more than made your money back on a monthly basis. All this feeds into how much “wallet share” the company can capture.

It's important for the pet, but it's also about share of wallet. This drives share of wallet. If you look at Vital Care, they spend 3x more than your average pet parent. $330 million for each point of share of wallet, Vital Care is a proof point. I have multiple proof points of how we drive share of wallet with our ecosystem strategy, and we are just getting started.

Other Benefits

Humanization of Pets → Recession Resistant

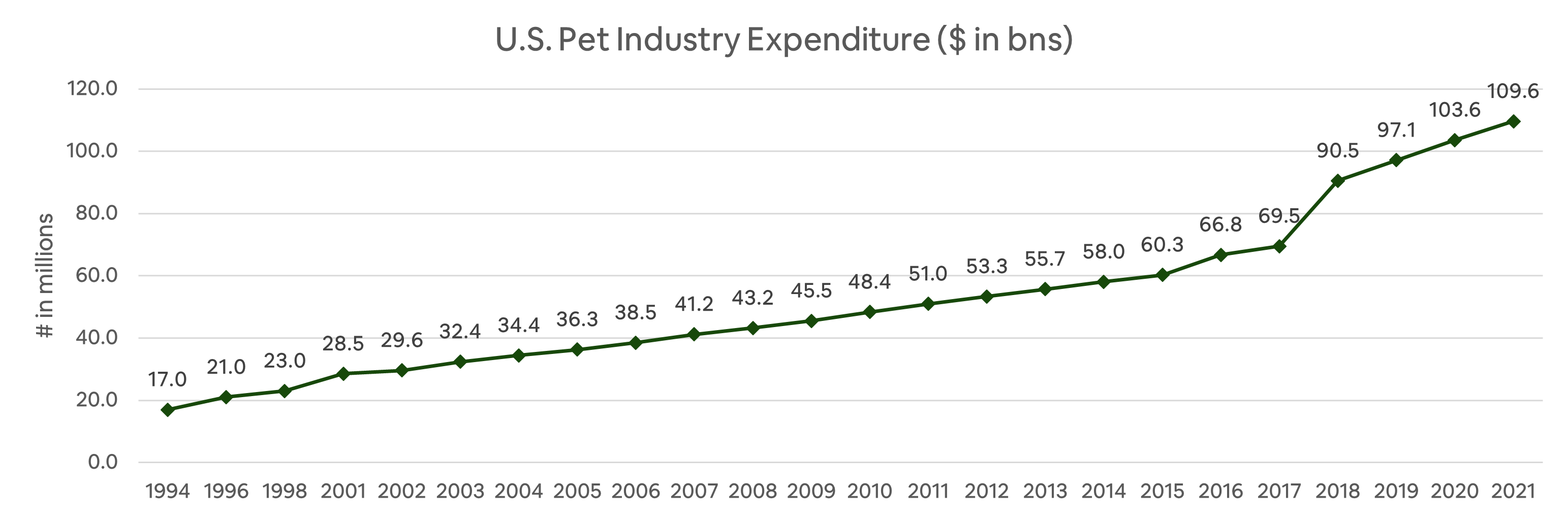

These days, Americans have become a nation of pet owners instead of parents. According to one survey, 80% of pet owners care for their pets like kids, 79% believe pets should eat the same food as people and 50% clothe their pets. Over 65 million American households have dogs. Only 35 million have children. There are about 4 million babies and 6 million puppies born in the U.S. every year.

Household penetration rates for pet ownership in the United States from 56% in 1988 to 67% in 2019.

“The U.S. pet care industry is a large, attractive growth market experiencing a significant acceleration in response to multiple secular consumer themes. Due to its non-discretionary nature, the market has demonstrated a long-term track record of consistent growth and resilience throughout economic cycles. From 2020 to 2024, the industry is expected to grow at a 7% CAGR, driven by steady, predictable growth in the underlying pet population coupled with strong tailwinds associated with pet humanization and COVID-19.”

Rover actually put out a very detailed report on pet ownership spending which includes inflationary pressures.

What’s also great to add is a recession-resistant component to the industry. Due to the essential, consumable nature of pet care, the industry has demonstrated resilience across economic cycles, as evidenced by the strong industry performance, spending even grew during the past two recessions: 29% during the 2001 recession and 17% during the 2008-09 recession.

Pricing Power

A fear going on in the current market involves inflation and just what will happen if it runs too hot for too long. Well, in the pet industry, given how pet parents treat their pets, there seem to not be as many issues when it comes to spending. Pulled from Petco’s recent transcript,

“On pricing, given our larger percentage of higher-end pet parents, customer demand remained largely inelastic in the quarter, where we realized favorable impacts from the pricing actions we took in both Q3 and Q4. In aggregate, we did not see a decline in product unit volumes for impacted SKUs.”

Additionally, upon our own research, it seems that many would reallocate spending from other areas in their life to continue giving their pet the “best life” they can while they can. This means that many have admitted to cutting key areas of their own life for their pet and also shifted spending in one area of their pet budget for another (ex, accessories to treats/toys/etc.).

The regular theme here is that many treat their pets better than themselves, relatively speaking.

Financials

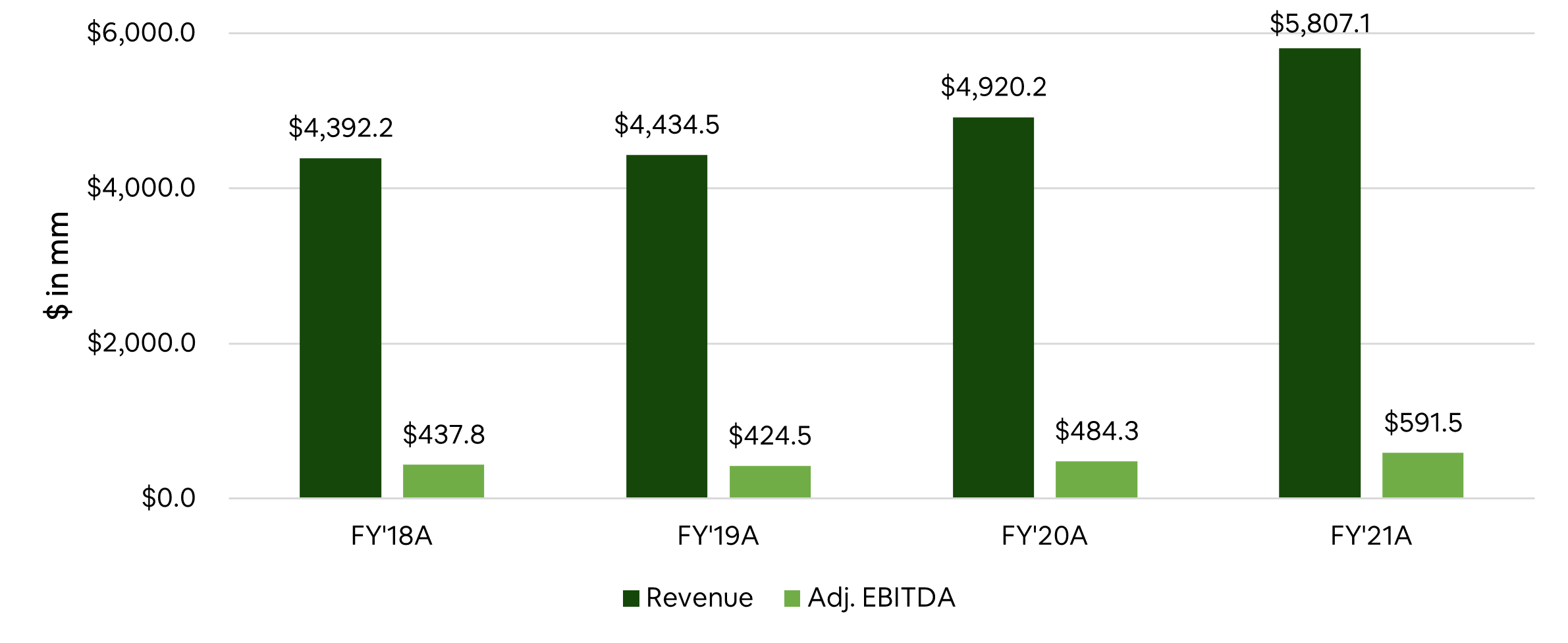

For some time Petco was experiencing a sense of stalling. Their revenue actually grew by -1.3% from 2016 to 2019. However, with the investment in digital and other areas, the company has been able to capitalize on its investments growing 31% on a 2-year stack (2019 to 2021).

At the same time, the company has also managed to increase adjusted EBITDA margins from 9.6% in 2019 to 10.2% in 2021 and grow EPS from -$0.07 in 2019 to $0.28 in 2021.

What’s great to add on is that given that the company IPO’d from a sponsor, they’ve managed to reduce leverage from 3.2x in 2020 to 2.5x in 2021 leaving them better situated to handle rising FED rates. The company has also managed to generate FCF in the last two years and improved a little under 10% this last year alone to ~$119 million.

A Misunderstood Stock

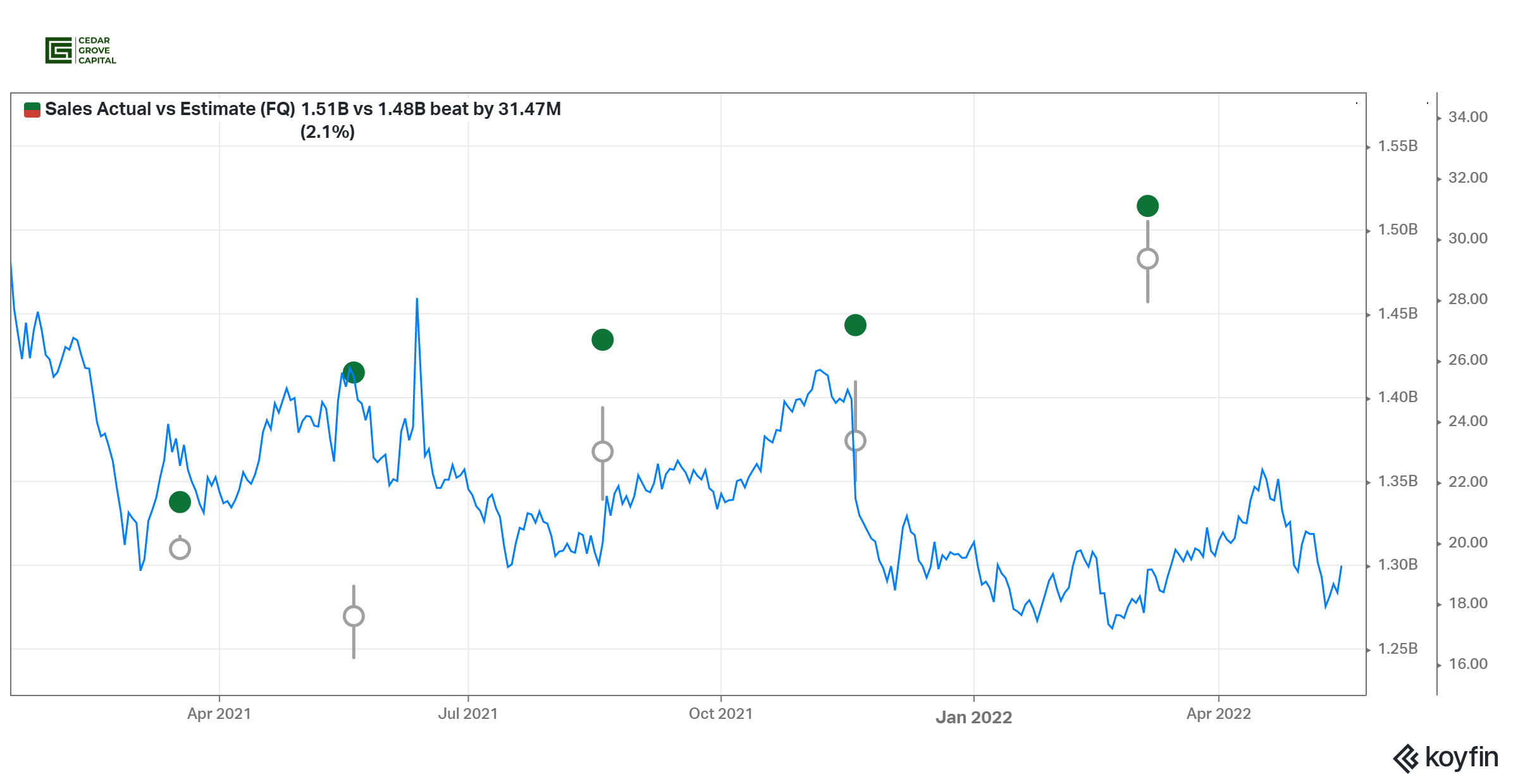

Besides the tailwinds that are helping the company and all the strategic initiatives that management has undertaken, the market hasn’t given it the recognition it deserves. To be fair, the biggest issue the company was facing in 2021 was exactly what Chewy was going through, a deceleration from a pull-forward in pet sales due to COVID. However, the company did the opposite (below).

Beats and Raises

While Chewy was facing a deceleration, Petco has been able to beat and raise 4 consecutive quarters in a row, and yet the stock has not been able to break past its $26 high (excluding meme squeeze).

Multiple Re-Rating

Besides the beats and raises, the company is still being treated as a traditional retailer that had a one-off benefit from COVID. Because of this, it’s fallen in the ranks alongside Chewy and Bark Box.

However, I believe that with all the improvements that the company has made over the years, it should not be treated like the other pet companies but rather other hardline retailers that have made digital improvements to its retail footprint.

With that being said, I believe that the company should be trading more in line with a Home Depot or a Tractor Supply Co.

They have made great strides in improving their digital business and overall footprint with their customers.

My Thoughts

One of the fastest growth areas for the business is services, veterinary services take part in that. They help fortify the ecosystem and boost customer retention and wallet share by getting customers in the door and cross-selling.

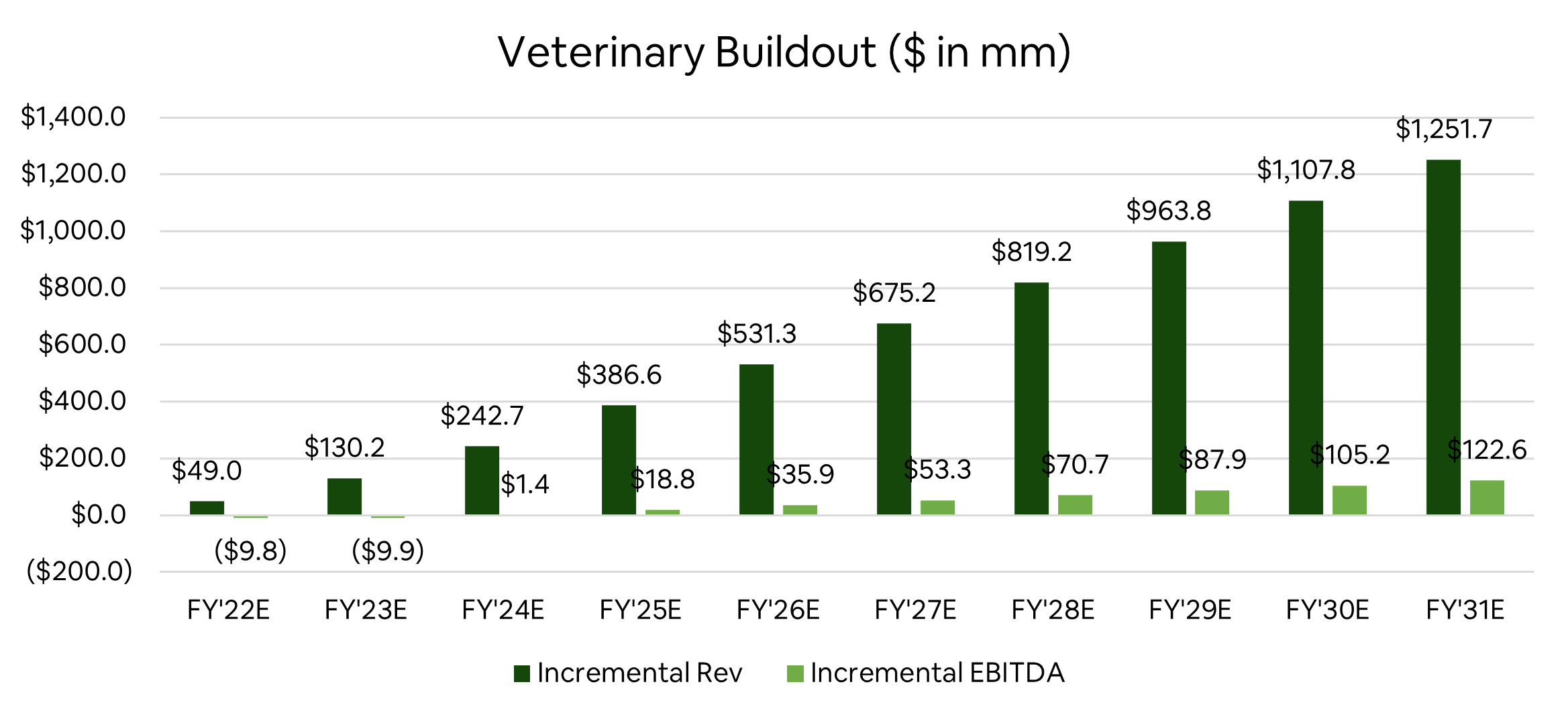

Vet Buildout

To paint you a picture of how I’m viewing this, I’ve modeled out the below in incremental revenue and EBITDA going forward. I’ve assumed ~70 new openings a year with each hospital generating ~$2M in AUV (this accounts for a blend between suburban and urban Petcos) and achieving 12% EBITDA margins by year 4 which also accounts for the ramp-up period and any pre-opening expenses.

Factoring in that, we can expect ~$1.3B in incremental revenue and ~$36M in incremental EBITDA by 2026E.

Valuation

Given the fact that Walmart and Target both reported poor earnings on a backdrop of a build-up in inventory and what appears to be softening in consumer spending coupled with freight costs, the stock sold off 15% yesterday.

Aside from near-term headwinds and dramatic price movement, long term the company is making the right moves to set it up for long-term success. With that said, 2022 is difficult to navigate so we’ll base numbers off of 2023E.

With the build-out of animal hospitals, moves to increase margin through cross-selling, and incentive to drive sales at the store level, we think topline growth of ~7% over the next two years while achieving 10.4% EBITDA margins in 2023E is reasonable.

This all relies on the resilience of the pet owner (which through our research is strong), how fast inflation can come down, no inventory build-up issues, and if we do or do not enter a recession.

Assuming the above and with a multiple re-rating closer to the 3-year historical average of Home Depot HD 0.00%↑ and Tractor Supply Co TSCO 0.00%↑ of about 14x 2023E EBITDA, you arrive at a $26 price. If the company is able to hold up in the near term (aside from the recent Target collateral damage), retracing to just over $20 could be in the cards by EoY 2022.

Overall, we’re bullish on Petco's management execution and the company being the best of publicly available US pet companies by fortifying its defensive moat and capturing more share in e-commerce and pet spending overall.

Until next time,

Paul Cerro | Cedar Grove Capital

WOOF: Banking on the Pet Industry