I never knew that Build a Bear (BBW) was actually a publicly traded company until the start of this year. In fact, I didn’t even know the company was still around. It was a store that I grew up with over two decades ago and by coincidence, heard a pitch on it back in January by Strat Becker. He discussed the company and his long thesis via a Commonstock pitch to Ross Klein, CIO at Changebridge Capital and it definitely got my attention.

I opted to forgo pursuing the stock further at that time because I felt all of Strat’s LONG points were priced in. However, what we all agreed on was that this company is relatively cheap, but it wasn’t getting the price it deserved on the public markets. So what did we all think was an obvious solution? Take it private.

TL;DR

The company has executed well on new store concepts and low labor-intensive revenue streams that helped accelerate growth

Despite all the strategic growth that BBW has executed over the years the lack of market coverage and general knowledge of the co has left it invisible

A few activists have made great examples of how BBW can deliver increased shareholder value while the stock price is depressed

Should public markets continue to fail, a leveraged buyout would provide triple-digit IRR and attractive MOIC in a few short years

Why the Equity is Undervalued

Company intro

Build-A-Bear Workshop (“BBW”) found its roots in the mall providing a unique experience to kids. Today, the company has an increasingly diversified physical footprint while prioritizing the expansion of its use case and leveraging its web presence to target adult customers.

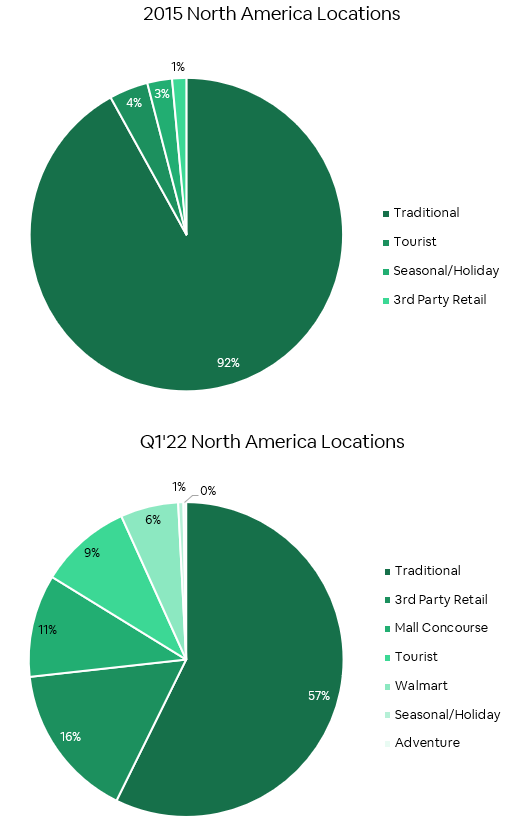

Of the company’s 370 stores in North America today, under 58% are traditional mall stores, a steep decline from 92% in 2015. This shift is being conducted to diversify the company’s physical footprint and avoid potential harm from struggling mall foot traffic by rotating to areas where foot traffic is rising.

Driven by high lease-optionality, BBW has been downsizing its mall presence by closing/replacing unprofitable full-sized mall stores with 200 sq ft concourses, opening stores in high-traffic tourist areas, partnering with third parties and other retailers, and by creating new non-mall store designs.

The company has also grown its share of sales to tweens, teens, and adults to over 40% of sales (ages 9+). This has been driven in part by online sales which are now about 20% of sales compared to 4% in 2015. The company has successfully prioritized targeting older customers for digital revenue and teens/adults make up the majority of end customers in this segment.

Growth Strategy

Increasing Ticket Size

The innovation in store locations has also come with increased product depth that enables upselling to customers. Add-ons including custom sound effects, scents, beating hearts, accessories, and props are all upsold to customers throughout the “bear-making” process as their lower input costs raise margins and create operating leverage within the business.

This has been seen from the company’s average transaction size growing by over 33% to $53.33 from 2013 to 2021 with gross margins increasing by 1120bps in the same period.

Licensing + Media

One of the drivers for higher transaction values has been the company’s licensed products which generate 30%-50% of the company’s sales in a given year. Licensed products sell at a premium price point and multiple releases from the same franchise (such as the Pokemon Eeveelutions), encourage repeat purchases from collectors.

The company is also beginning to lean into the creator economy through licensing deals with the popular toy review YouTuber Ryan’s World and TikTok duo WeWearCute.

Build-A-Bear is also growing its selection of owned IP products to reduce business cyclicality caused by third-party content release schedules.

Leveraging its media channels, the business released its first movie, Honey Girls, last year. Originally released in theaters and now on Netflix, the movie boosted Honey Girls sales by 20% with an average transaction value of $90 vs the company average of $53.33.

The business also has a significant presence on iHeart Radio with over half a million monthly listeners.

Product Pipeline

Outside of media investments, the company has a robust product pipeline that sees new concepts in stores within a year and uses online soft launches to gauge demand before making large inventory investments. This effectively limits product development risk by not doing full-scale launches each time.

Some of these products like the “Pink Frog” and “Axolotl” have become significant TikTok trends and sell out at a rapid pace, and recent in-person channel checks/conversations with store employees indicate an increased ability in selling original products. Secondary markets for these animals have also ballooned on eBay where that Pink Frog goes for $80, used. Over 3x the retail price.

Furthermore, online trends such as “The Build-A-Bear Date” have expanded the in-store customer to increasingly include teens and adults.

Love in a Box

Additionally, BBW is further diversifying its revenue streams and increasing margins by investing in low labor and low fixed cost growth. It recently launched an online gifting service, Heartbox, which targets a higher price point customers and may have sales over $5 million next year.

The company also started a subscription delivery service, Cubscription, which charges $29.99 on a quarterly basis. Already making up about 20% of the company’s retail business, these new e-commerce initiatives further enable operating leverage as 70% of the company’s online orders are fulfilled in-store locations, minimizing overhead and incremental labor costs.

Vending Machines

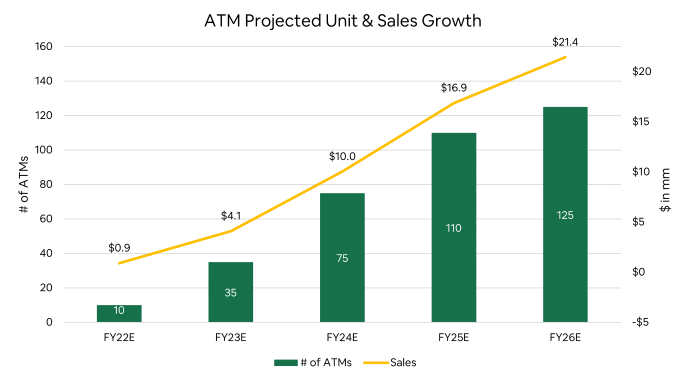

Even with notable online launches, the company’s most public-facing new project has been the introduction of automated vending machines. Placed in high-foot traffic and situation-oriented locations such as airports and children’s hospitals these machines generate sales from people who want to get an impulse gift while on the move. Starting with a single pilot machine in JFK airport less than a year ago, this concept will have 10 machines in operation by the end of this year.

More than half of these machines will be in airports through a relationship with Hudson Group which will ramp to 25-50 airport locations in the next 18 months. In addition, the company will be to selling premade Build-A-Bear products at more than 10 other Hudson Group locations in a wholesale model with plans for future expansion.

This will potentially add over $10 million of revenue and $2.5 million of EBITDA (margin of 25% vs company level of 15% in 2021) to fiscal 2024 results with sales per sq foot over ten times higher than the company average.

Store Innovation

The company is also opening 20 non-mall locations this year with a mix of company-owned and third-party locations. This includes the new Build-A-Bear Adventure store concept, which will provide a broader customer experience and serves as a localized distribution hub for online orders. A revamp of the web experience and CRM is also being made to bring it up to par with modern standards.

Importantly, all growth drivers are capital-light investments, with company-owned stores costing between $300k and $500k to open, third-party stores having no cost, vending machines costing an estimated $50k, and e-commerce/CRM upgrades costing an estimated $1 million means that BBW CoC returns are attractive.

For example, ‘22E CapEx for all growth initiatives and maintenance of existing operations is forecast to be 2%-3.25% of total sales, emphasizing the capital-light nature of the business.

Valuation

The apparent prospects for continued growth with expanding margins appear at odds with the valuation the market assigns to Build-A-Bear.

Despite the company’s success in diversifying its operations, almost 20% domestic sales growth in Q1, ROIC of over 25%, and no debt with a net cash balance worth 10% of the company’s worth, the market still prices the company at a dirt cheap level at under 2.6x 2022 forecast EV/EBITDA.

BBW is priced as if it’s facing significant issues like other retailers, but its performance indicates the opposite. EPS is almost double its peaks in 2007 and 2015 with its topline growing at double-digits without any stimulus in play.

Importantly, margins have also seen significant expansion with the operating margin 700bps higher than any other point in the past decade.

FCF is currently held in check by inventory investments (~$2/share of FCF in the LTM) but will flip to being an additive to cash flow by the end of this year as better supply chain and cost visibility will allow the company to increase inventory turns.

The company’s healthy balance sheet has allowed it to return cash to shareholders, giving back over 12% of its market cap in buybacks and a special dividend from December 2021 to May of this year. The flip in inventory investments to cash flow will increase this ability further, and activists are pushing for larger buybacks or a tender.

Trading at under 5.5x 2022 estimated P/E with growing sales and profits at double digits and a long-term runway, this doesn’t seem unwarranted.

**In section two of this post, an activist investor also visually highlights what multiple the company should be and the assumed price from said multiple.**

Why It’s Not Getting the Recognition it Deserves

The reason the company gets no credit in its stock price for great execution appears to be caused by a lack of coverage preventing more up-to-date information from being accurately priced. Non-sponsored coverage hasn’t existed since 2015-2018 when the business’s concentration in malls and lack of online sales left it prone to the mallpocalypse, becoming a value trap.

This misunderstanding of the company’s position is further impacted by concerns industry-wide about inventory markdowns as many retailers face an inventory glut. To this point, it’s important to note that the mix-and-match nature of Build-A-Bear’s products sharply reduces obsolescence risk. Add-on products like accessories and sound effects have no reliance on what “bear” they’re in, so any risk of them being marked down is inherently reduced.

Lower liquidity can also have an impact with under 2% of the company’s market cap (~$5 million) trading on an average day, though this is arguably tied to the lack of coverage on the company.

With under 58% of North American locations in a traditional mall format and 20% of sales now online, the company has significantly improved its physical footprint and sales makeup, something which is reflected in higher operating margins and successful rollouts of new store concepts such as the concourse and store-in-store agreements.

Growing sales and profits by double-digit percentages with no stimulus show in our opinion that the stock is significantly undervalued.

Risks

Since this is a retail stock, that automatically means that there are certain risks associated with the business that is unique to BBW itself but also fall into the trend with other retailer issues this year.

Employee attrition - The company is dependent on well-trained staff to upsell during purchases, increased attrition may harm operating leverage and margins by not promoting high-margin add-ons

Reliance on licensed content - In a given year 30%-50% of sales come from licensed IP making the company reliant on third parties for the timely release of new content and also leaves it exposed to potential contracts ending (ex. HAS with Disney)

Concentration in malls - The company must continue diversifying its store portfolio away from malls, delays/issues with new store formats may harm this transition and cause a slowdown in growth

Recession - Given that this company is in fact a discretionary company, any decline in consumer spending - whether due to inflation or recession - could negatively impact the company

How BBW Can Improve Shareholder Return

If we take a look at what more management could do to boost shareholder value, the obvious answer is to be more aggressive with buybacks. Since December 2021, BBW has bought back 840,401 shares for a total price of $14.1 million. The current share buyback program is near exhaustion and could mean that the BoD might consider instituting a new buyback program.

In the meantime, given its zero debt balance, cash on hand, and growing FCF, the company has been approached to do more.

Let’s start with Kanen Wealth Management.

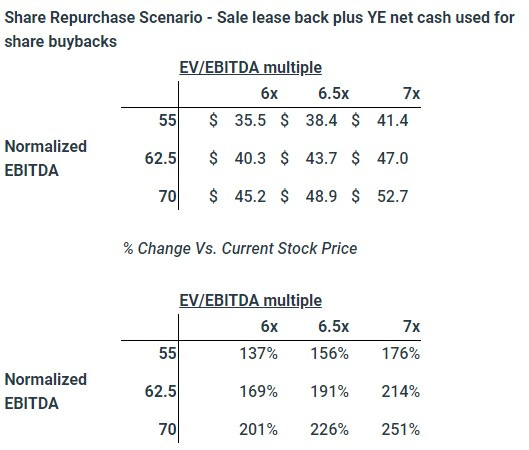

Kanen Wealth Management is a fund that owns a little more than 6% of the total shares outstanding as of Jun 30, 2022. Kanen has been an activist for quite some time and even used to have a seat on the board. In July they approached management with a share buyback plan that would reduce the number of shares by ~6.2 million (~40%) and allow existing shareholders to own 67% more of the company.

Here’s how they thought through the math.

Valuation in a sale-leaseback of at least $31M

Associated lease expense of ~$1.8M

Co has the opportunity to sell (and leaseback) this asset at ~17.2x earnings and repurchase stock at ~3.2x EBITDA

This would be accretive to earnings per share by ~11%

They also mention that they believe that the company’s net cash position could improve to ~$75 million over the next 6 months bringing the total net cash position to ~$105 million ($75 + $31 in RE) which is how they get to ~6.2 million in shares repurchased.

A more recent call of activism is from Cannell Capital, which owns 10.7% of the stock, also calling for more aggressive buybacks. They’ve had a longstanding role in BBW including prior board nominations. Cannell Captial believes that the BoD are asleep at the wheel and don’t know what they’re doing.

In their proposal, they outline a few things:

$26 million of cash on the balance sheet

Borrowing $25 million at 5% interest (based on their estimates)

FCF for this year of ~$30 million

A sale-leaseback of their Ohio distribution center yielding ~$35 million

“BBW stock is trading at just 6x 2022 estimated EPS, its lowest level in about 18 years. By our math, if BBW were to monetize its real estate assets and take net leverage to just 1x through a tender at $17 per share, 2022 earnings per share would grow 110% inclusive of incremental interest and leasing costs.”

“On July 21 Cannell Capital talked to BBW and urged its Board of Directors to conduct a modified Dutch tender for BBW's common stock. They believe that if they don’t do something soon, a board shakeup is needed.”

For context, a Dutch Offer is just a solicitation to buy shares at a given point in time based on the best offer price of said duration whereas a share buyback program allows for a certain amount of capital to be used over time at management discretion which could allow for more favorable/unfavorable prices.

Both have valid points but just go about them in different ways. If the stock isn’t moving, then take advantage of the subdued stock price to reward shareholders at the current levels. Will BoD do it? Maybe, but we’ll see if they arrive to this conclusion on their own come the next earnings release this week.

Take it Private - LBO

If public markets won’t give it the recognition it deserves, then take them private.

For the final leg of possible solutions here, perhaps BBW not being a public company anymore might be in its favor. Here’s where Strat and I believe that BBW could make for a great leveraged buyout and why PE firms should consider it.

First, what makes for a good leverage buyout?

Strong FCF generation

Some type of moat or favorable unit economics

Little to no debt

Undervalued (assets and/or the business itself)

We believe that Build-A-Bear has all of this. This section is going to highlight why a hypothetical take private of BBWmakes sense but by no means is it a complete LBO model. We’re not doing the work of PE if we’d be the ones holding the equity that needs to be bought out.

So where do we start? What can PE pay? Given that two active investors have publicly written to the BBW BoD about how to return more capital to shareholders, selling the company without a sizeable premium has little chance of going through.

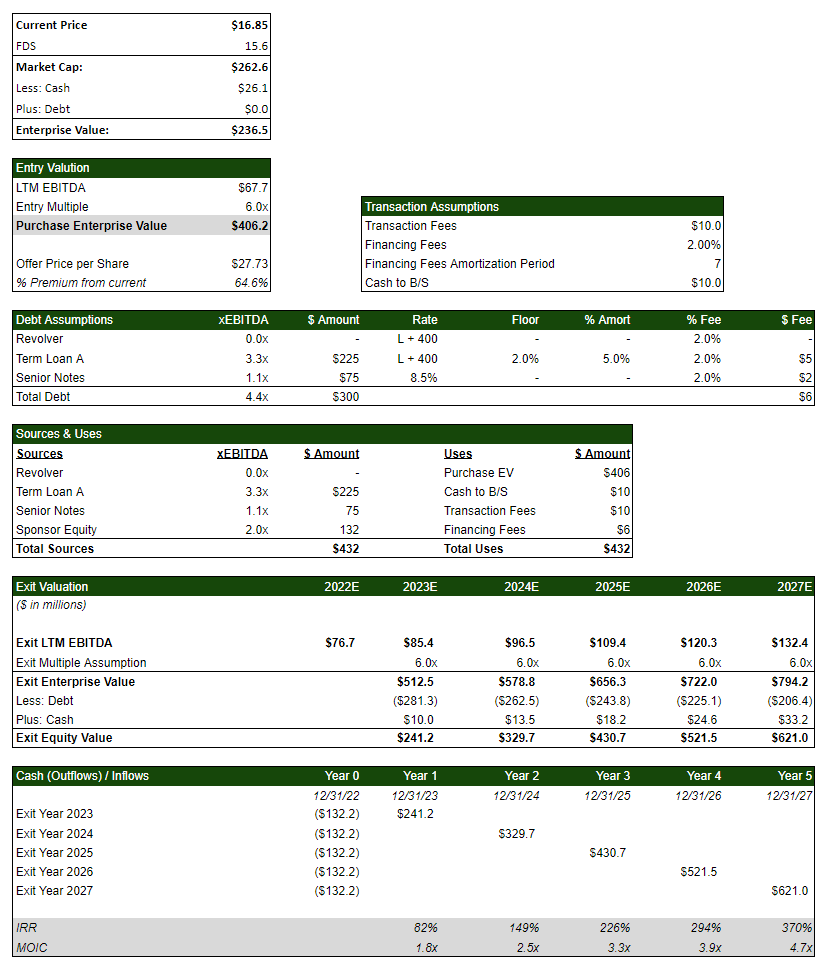

For this reason, based on LTM EBITDA of ~$67 million, and assigning a 6.0x multiple, we arrive at a take private EV of ~$406 million, or a share price premium of ~65% based on Friday’s close.

Now there are tons of ways to go about funding this and deciding what level/type of debt you’d like to use. For our purposes, given how the company has no debt, net cash of $26 million, and substantial FCF generation, we opted for a traditional revolver, a 7-year term loan, and a senior note offering.

Given all the fees, transaction value, and cash to be placed on the balance sheet, we’re looking at a total take-private cost of $432 million. Don’t let this worry you though, with the FCF that the company generates and the expectations of continued financial growth, the company can more than service its interest requirements.

If we look at what PE could make on the transaction, take a look at the table above. Mind you, this is not perfect and many different assumptions and iterations can be taken place that affects almost every aspect of this rough output.

Based on Strat’s assumptions for EBITDA, in just 5 years, we see it grow from ~$77 million in ‘22E to over ~$132 million in ‘27E. Almost doubling in that time. Given how well the company is growing, factoring in zero multiple expansion, and paying down only the required debt each year, a PE firm can make a pretty penny.

Based on the initial sponsor equity of $132 million, 5-year IRR (in the event of a sale) would be ~370% and MOIC of ~4.7x. These numbers should have any PE shop’s mouth drop to the floor.

Any PE bros out there reading this should consider building out their own model for this and take it to their boss **cough cough** L Catterton.

Why this hasn’t happened yet? The biggest problem is the lack of skin in the game from the BoD and CEO having a cushy comp package that despite her over 3% ownership of the stock, the two parties may show an unwillingness to sell.

A PE shop would have to convince them of the deal being worthwhile to execs rather than just shareholders. This in and of itself could be a hindrance to a deal taking place.

Selfish…

Conclusion

Given how the company was being priced as if it were about to go bankrupt in 2020, the “Teddy Bear” company has been doing quite well under the hood despite the market hasn’t given it the recognition it deserves. That doesn’t necessarily mean that investors have missed the boat from the lows, but that the upside is still very much there.

While we’ve outlined what’s been going on with the company underneath, options that can increase TSR, and a long shot of an LBO, this micro-cap stock should warrant further attention from those interested in something clearly undervalued.

At worst, you end up buying a modern stuffed animal for someone you love.

If you enjoyed our research and would like to subscribe, click on the individual buttons below.

For Cedar Grove Capital, you can click the “Subscribe Now” button.

For Strat Becker’s newsletter, click the button below to be taken directly to his Substack.

Until next time,

Paul Cerro | Cedar Grove Capital

Paul Cerro Twitter: @paulcerro

Strat Becker Twitter: @stratbecker

BBW: Stuffed With Unrecognized Value