Good morning everyone 👋🏼!

Welcome to Cedar Grove Capital — your source for actionable insights, industry deep-dives, and single name coverage in the consumer(tech), and cannabis industries. If you are new, you can join below. Please hit the heart button if you like today’s newsletter and reply with any feedback.

Foreword

The start of 2022 has not been kind to many of us. With a complete sell-off in technology names and fear of more FED rate hikes than expected, investors have no clue where to go from here. The unfortunate part of all this is that panic selling begets panic selling and it creates quite the negative snowball effect.

With everything looking to be deep in the red, there are plenty of opportunities to pick from if you’re looking to deploy cash. One of these opportunities that I’ve noticed is in RH. Let me tell you why.

Summary

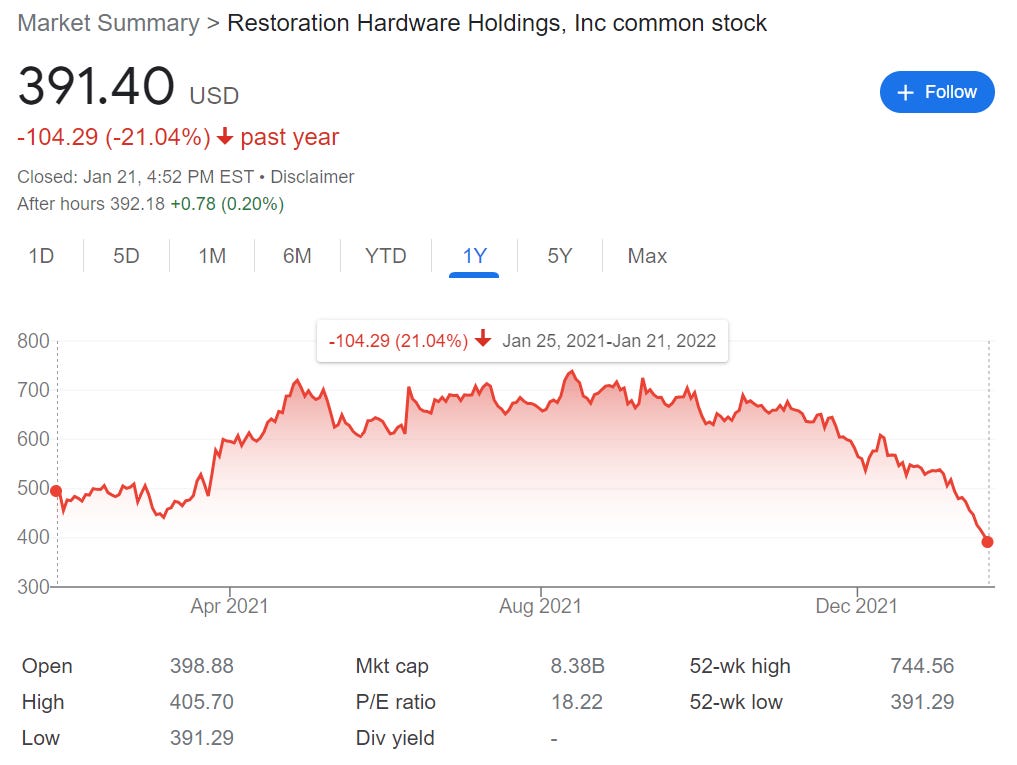

Despite the company consistently exceeding consensus estimates over the last two years, the stock has drastically receded from its mid-$700s high last year to sub $450 this week

The company’s stock is attractive given its currently trading at a P/E multiple less than it has historically

RH has been able to navigate inflationary and supply chain worries over the last year is shown in their financial performance

Any shares under $400 are quite the steal and should not be ignored for the long-term investor

Quick Recap

I initially wrote about RH RH 0.00%↑ back on July 20th of 2021, (can find the article here - RH: Nothing Stopping this Bullet Train) when it was trading at $646.11 and I estimated that it could be worth $754. Well, it didn’t hit that price but it came pretty darn close to it ($744.56). Since then, the company has continued to beat expectations and execute well on management long-term guidance. To quickly bring you up to speed, let’s start with who they are.

Who is RH?

RH (RH), formerly known as Restoration Hardware, is a luxury home furnishings retailer. They sell things like furniture, lighting, textiles, bath-ware, décor, and outdoor and garden furnishings. They sell their goods in their various retail locations (design galleries, like the one shown below), online, and through their catalog.

While they are a luxury retailer, what exactly does luxury mean? Well, a leather couch can push upwards of $16,000 if that paints you a picture. If it’s not evident yet, they clearly cater to a wealthier type of clientele that can afford couches of that price tag.

But RH is different than many home furnishings companies in that it is incredibly simplistic in how it runs its business model. It does not sell any seasonal products, does not derive its inventory based on fashion trends, nor does it position itself as a mass-market brand.

Things that many brick and mortar retailers try to get in early on and ride the wave as long as they can, which if you think about it can leave them with some serious inventory surplus risk.

Why I originally went long

Unlike other retailers in general, RH had a few things going for it that really set it apart from the rest.

1) Strong unit economics from galleries

Looking at the above design gallery, it’s nothing less than bougee (really nice). Design galleries are huge, roughly 45,000 - 60,000 sq. ft. with some (Meatpacking, NYC) of upwards of 90,000 sq. ft. This trumps in comparison to their legacy stores which were on average, a mere 7,500 sq. ft.

So how does this translate? Well, design gallery economics is far superior to legacy stores, yielding on average +100% sales lift, and +10-20% direct lift, significantly expanding RH’s market share.

The company estimates that these new design galleries will deliver revenues of $5 billion to $6 billion in North America alone. Not bad.

Once the pandemic-related interruptions have subsided, plans of 5-7 openings annually will help RH reach its over 70+ gallery target.

2) International expansion

Like many companies who started off in the US, eventually, to continue expanding, you have to go abroad and RH has its eyes set on Europe. According to the company, the total European addressable market for luxury furniture is estimated between ~$40-$43 billion and is highly fragmented. Pulling a quote from the CEO,

“We believe that RH has the potential to become a $20 billion to $25 billion global brand in its current form and possibly larger if aspects of our ecosystem become meaningful revenue streams. Our view is the competitive environment globally is more fragmented and primed for disruption than the North American market. And there is no direct competitor of scale that possesses the product, operational platform or brand of RH.” - Gary Friedman, CEO

When I originally wrote the post, the company was planning on opening up locations in the UK, France, and Germany.

3) Margin improvement

The company was targeting to hit and maintain operating margins of 25% or better and internally, efforts to improve margin through operational efficiencies were being executed in a spectacular fashion.

Back in July, RH stated that it was focused on continued optimization of its operating model driven by:

Higher AUV mix as RH continues to elevate its product assortment.

Vertical integration of home delivery – fewer returns and lower transportation costs.

Fixed cost operating leverage as the new design galleries carry significantly higher productivity levels.

Transition to a capital-light real estate model (sale-leasebacks) – lower rent expense, and depreciation.

Easing headwinds from hospitality and waterworks de-leveraging over the coming years.

This strategy is proving to become a reality as is shown in their quarterly financials.

4) Recession-proof(ish)

What’s also a plus that you shouldn’t discount is the nature of this type of consumer discretionary space. When the economy slows or enters into a recession, many investors believe that consumers will pull back on most spending which means retailers get massacred. This is not entirely true when it comes to RH.

RH appears to be resilient to market swings because it caters to wealthier shoppers who are less exposed to economic downtrends.

In fact, the wealthy are always more likely to win in recessions, as NYU economist Edward Wolff has found. During recessions, wealth and income inequality grows. And as economist Hilary Hoynes and others have discovered, poor and indebted households are affected much more by business cycles.

Plus, RH serves customers who have money to spend, so it doesn't rely on discounting inventory during a slow economy to drive sales.

So with so much going for it, why has it taken a nosedive down the valley of death like everything else? Well, let’s start with my current take.

Reiterating LONG Thesis

RH was a stellar winner during COVID, rising over 780% from trough (March 2020) to peak (August 2021). However, over the last year, the stock is down 27% YTD and has reached a new 52-week low.

But this unwarranted decline has led to quite the buying opportunity for investors. In the next few topics, I’ll explain why the future still looks incredibly bright for the company.

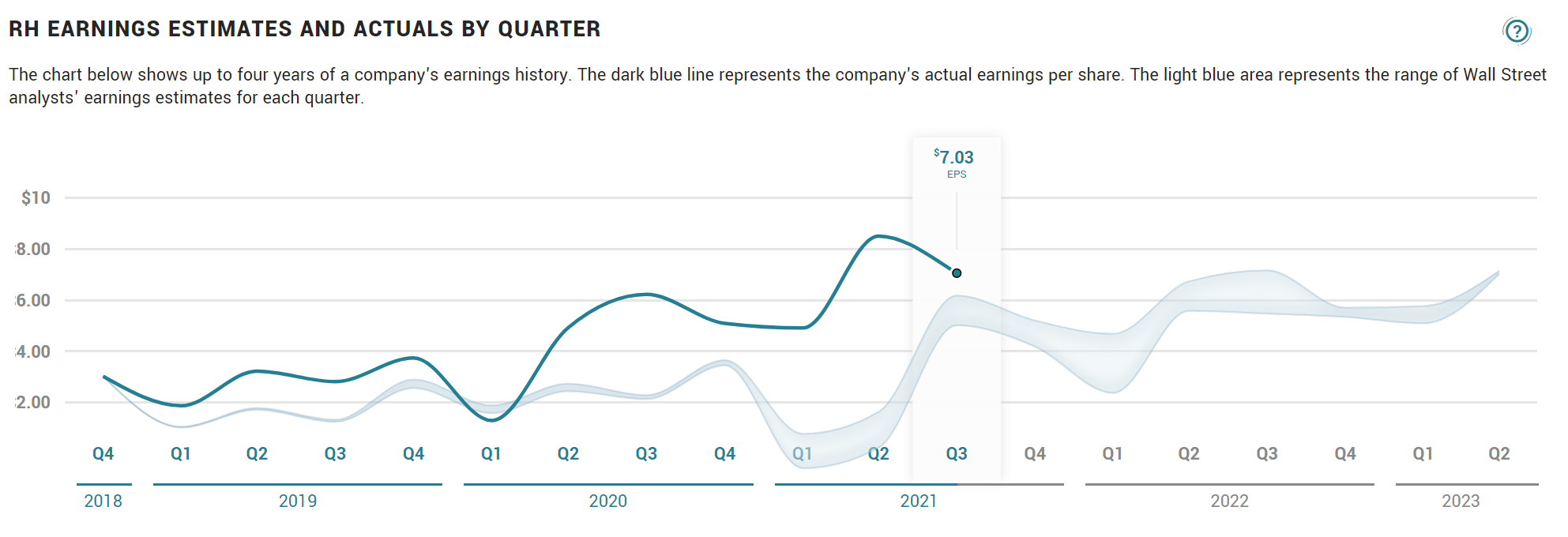

1) Beat. Beat. And Beat Again.

Not sure why investors bet against this company but I firmly believe that those who do truly do not understand it and have never actually walked into one. If you haven’t yet, you should because they are insanely nice.

Regardless of how I feel about the naysayers, RH has consistently beat Wall Street estimates time and time again. In fact, the company has beat estimates on both the top and bottom lines (revenue and EPS) almost every quarter dating back to Q1’19 except for one. That’s 10 out of the last 11 quarters! And curious to know which quarter they missed? Well, it happened to be the quarter ending March 30th, 2020, and it was a ~$40 million miss on revenue. Hmm, wonder why that was?

To add more weight to this point, over the last eight years, the company has grown non-GAAP EPS at a 21.3% CAGR. Impressive!

This continued financial performance fits in well with what I mentioned previously, which is the company being recession-proof(ish). Even at the height of the pandemic, consumers were still spending their money lavishly and RH happened to be a strong beneficiary of the bountiful surplus in American wallets.

If you’re looking for a company that not only a) has earnings, but also b) a strong track record of proving investors wrong, I’d say RH is a top contender.

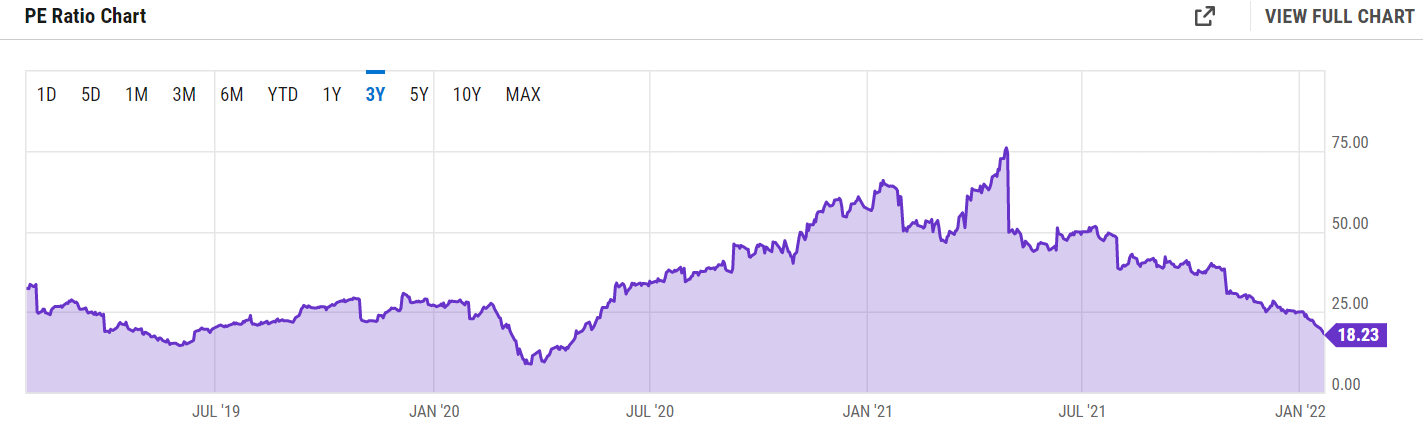

2) Trading under its historical P/E

Another point that I want to highlight is its valuation. The good thing for RH is that they have earnings so there will be none of this P/S valuation methodology BS taking place for this company. No sir. We’re working with solid earnings and can look at P/E ratios in order to help us determine how it’s being benchmarked.

Looking at the chart above, as of the close on January 21st, 2022, RH was trading at a P/E ratio of 18.2x. So let’s put what this means into context. 18.2x for a P/E ratio isn’t all that bad when you consider the company’s median TTM P/E ratio over the last three years of ~25x. This three-year time frame consists of a FED funds rate that was over 2% for half of 2019 and ~1.5% for the second half of the same year before plummeting to near zero during the pandemic.

I’m briefly highlighting the company in a much higher rate environment but I’ll dive into that more soon.

What’s also key to note is that even though the company’s current TTM P/E is lagging its historical median, it’s still well under the Consumer Discretionary Select Sector SPDR Fund (XLY) and the overall S&P 500 Index of 36.6x and 27.2x, respectively.

But Paul, this is all backward-looking, the market is forward-looking. Yes, I know but I still wanted to highlight this as one point to consider and will address this in a minute.

Why have investors lost faith?

I believe that there are three main reasons why investors have sold off this stock, again, without good reason.

Inflation → worries that higher input costs will eat into the company’s margin.

Supply chain issues → will cause delays in inventory and higher shipping and freight costs.

FED raising rates → higher rates means more interest expense.

Let me address all these three.

1) Inflation

So fears of inflation, which are pretty obvious at this point, have caused panic amongst investors who are selling their stocks off in response. However, the company has done well to not affect the margin efficiency it’s achieved over the years. To make sure margins don’t deteriorate, the CEO mentioned on the last earnings call that to an extent, they’ve passed the price increases to the consumer.

Yes, I'm not even sure price changes are over yet. So yes, there's still price inflation happening. And so we're going to continue to do what's fair and right and -- but we don't want to do anything that kind of undercuts the margin structure that we have….but everywhere it's happening. Restaurants crazy price increases and a lot of the input costs, and we're just doing what we believe is right and fair.

As our price is going up, we're passing them through. - CEO Gary Friedman

And to the point of how much are customers willing to pay as RH continues up the luxury ladder, Gary also responded with,

And so when you think about price elasticity, you've got to think about all of these things that we're doing and all these investments we're making that will render the RH brand more valuable, that will render our product more valuable and more desirable.

And yes, we think we're on a path in our industry that's not too dissimilar to the path of Apple, the path of Nike, the path of Tesla, the path of people who really, really built the best brands of their kind in their industries, and they became the best brands in the world….and that gives you a lot of pricing power.

And yeah, I agree with him.

2) Supply chain

Talk about buzzwords, that was of the many words that were on everyone’s minds during 2021 but, luckily for RH, they have an underlying trend that helps them greatly. Many consumers had to go about long wait times to get their goods than they usually had to in the past.

To put this into context, the Washington Post gave a great example of a puffer jacket and how long it was taking to reach consumers. The time to manufacture said puffer jacket was the same, but the time to ship jumped from 33 days in 2019 to 70 days in 2021. More than doubling during the pandemic!

But what does RH have under its sleeve that somewhat mitigates this risk? Even before COVID, they had longer wait times than traditional retailers. While smaller items were shipped out faster, their bigger ticket items like couches, etc. would take weeks. Their customers were almost kind of trained to wait for their goods to arrive which some could argue just builds up the excitement until your goods actually come through the door. Since customers were already accustomed to this, having to wait an extra few weeks isn’t crazy.

Additionally, ~20% of their goods are made in Viet Nam which had their whole country shut down for a while due to COVID. Though overall, their sourcing of products is diversified across many countries so there’s no single country risk when it comes to supply chains.

3) Rising rates

Another issue that everyone is well aware of is the FED raising rates and the market is now projecting four rate hikes in 2022.

With that being said, the obvious factor is that debt gets more expensive and the desire for investors to have an appetite for riskier investments subsides.

That being said RH does have a decent amount of debt, roughly $2.2 billion in LT debt and ~$150 million in ST debt. What I love about RH however is that it’s been able to take on debt quite often using 0% convertible notes, most recently in June of 2018 (which I was on back at Merrill Lynch) for $350 million. This allows them to essentially get a zero-interest bond with the option for the bondholder to convert at a specified price, in this case, $193.65. This gives the company access to cheap capital that doesn’t necessarily need to be exercised, though I don’t see why they wouldn’t.

Last year, the company took out a Term Loan for $2 billion with a maturity date of 2028 for LIBOR + 2.50% with LIBOR floor set at .50%. Not to get too technical but this is not that expensive of debt and is quite the typical rate for healthy companies that aren’t massive conglomerates.

My point to all this is that, yes, the company has debt on the balance sheet but even if interest rates were to rise, it wouldn’t put the company in any jeopardy. In fact, the company right now has an interest coverage ratio of 16.1x, meaning it generates more than enough pre-tax operating income to cover its interest expense.

Am I worried, not at all. RH has a proven track record of being able to borrow cheaply and is in a healthy position to pay back its loans.

Valuation

Back to the valuation portion which I know everyone is waiting for, if we look through a forward lens, we get a slightly different picture than what I mentioned previously. RH’s forward P/E (fiscal year ending January 2023) is at 15.6x, the S&P 500 Index is at 20x, and the Consumer Discretionary Index is at 25.9x.

Even if you switch to forward-looking, I estimate that EPS will be ~$26 in FY’22. If we look at the Consumer Discretionary average multiple, that gets you to $673 while using the S&P 500 Index average multiple gets you $520, or a 65.4% and 27.8% upside from yesterday’s close, respectively.

Stars are pointing north over here.

Closing Thoughts

RH is an amazing company and has an excellent management team that is executing on all levels to deliver maximum shareholder value. The company is trading down 43% from its ATH while more than tripling its EPS over the last two years. They have gone places and will continue to go places which is why I’m bullish on the long-term prospects of RH.

Until next week,

Cedar Grove Capital

RH: Too Cheap to Ignore at These Levels